00

Dear Founders, Investors, and Friends,

September was a notable month for digital assets in Europe. From the Sibos conference placing stablecoins at the heart of the global payments agenda to major European banks launching a shared Euro stablecoin initiative, institutional adoption moved from talk to execution. Meanwhile, Societe Generale entered DeFi, and across the Atlantic, the SEC unlocked faster approvals for crypto ETFs.

Let’s take a closer look at what happened, and why it matters.

Table of Contents

- Institutional Adoption

- Sibos 2025: Digital assets move to center stage

- Nine Banks, One Coin: Europe’s new stablecoin consortium

- Societe Generale pushes EUR stablecoin into DeFi

- U.S. Regulatory Update

- SEC streamlines crypto ETF approvals

Sibos 2025: Digital assets move to center stage

Frankfurt played host to this year’s Sibos, Swift’s flagship conference for global payments and financial infrastructure. And for the first time, digital assets weren’t just a side conversation. They were front and center, with the opening directly setting the tone: Swift CEO Javier Pérez-Tasso announced a blockchain-based prototype for 24/7 cross-border payments, developed with Consensys and supported by more than 30 major banks including JPMorgan, HSBC, and BNP Paribas.

What followed were many announcements that mainly revolved around the one thing most interesting to the payments industry right now: stablecoins. For example, Swift revealed it is piloting stablecoin-to-fiat conversions, while Clearstream – Europe’s leading post-trade infrastructure provider – announced plans to integrate Circle’s USDC and EURC stablecoins into its securities infrastructure, a clear signal that tokenized cash is starting to find a place in traditional financial systems.

Also, it wasn’t just what was discussed, but who. Just a few years ago, digital assets were the domain of innovation labs, often times with rather small budgets and teams. This year, though, the conversations were led by global heads of custody, treasury, and capital markets. That shift signals a clear change in mindset: traditional players are no longer exploring if blockchain has value, they’re figuring out how to deploy it. And how to do it at scale.

Nine Banks, One Coin: Europe’s New Stablecoin Consortium

But the fact that institutions are now seriously engaging with digital assets didn’t just become clear at Sibos. A few days before the conference, another major announcement came out of Europe: nine of the continent’s largest banks, including ING and UniCredit, announced a new consortium to launch a euro-denominated stablecoin, with the rollout planned for the second half of 2026.

While this isn’t the first bank-led stablecoin initiative, it is the first major collaborative approach.

And the logic seems pretty clear: a common standard is more efficient than fragmented issuance. As Floris Lugt of ING noted in an interview: “We also saw that if each bank would issue their own stablecoin, then they need to become interchangeable. That’s complex and inefficient. A lot of the benefits of blockchain are immediately taken away.”

The new stablecoin will be issued by a dedicated entity in the Netherlands, supervised within the Eurozone. Each bank will hold an equal stake, and the consortium remains open to new participants. Governance and reserve management are designed to ensure neutrality, scalability, and broad adoption.

Importantly, the project is chain-agnostic. No new network will be launched. Instead, the focus is on integrating into existing ecosystems, including decentralized finance (DeFi).

Initial demand is expected from corporates and institutions for use cases like cross-border and tokenized securities settlement. And when it comes to retail users, the main goal is to become a general means of onchain payments.

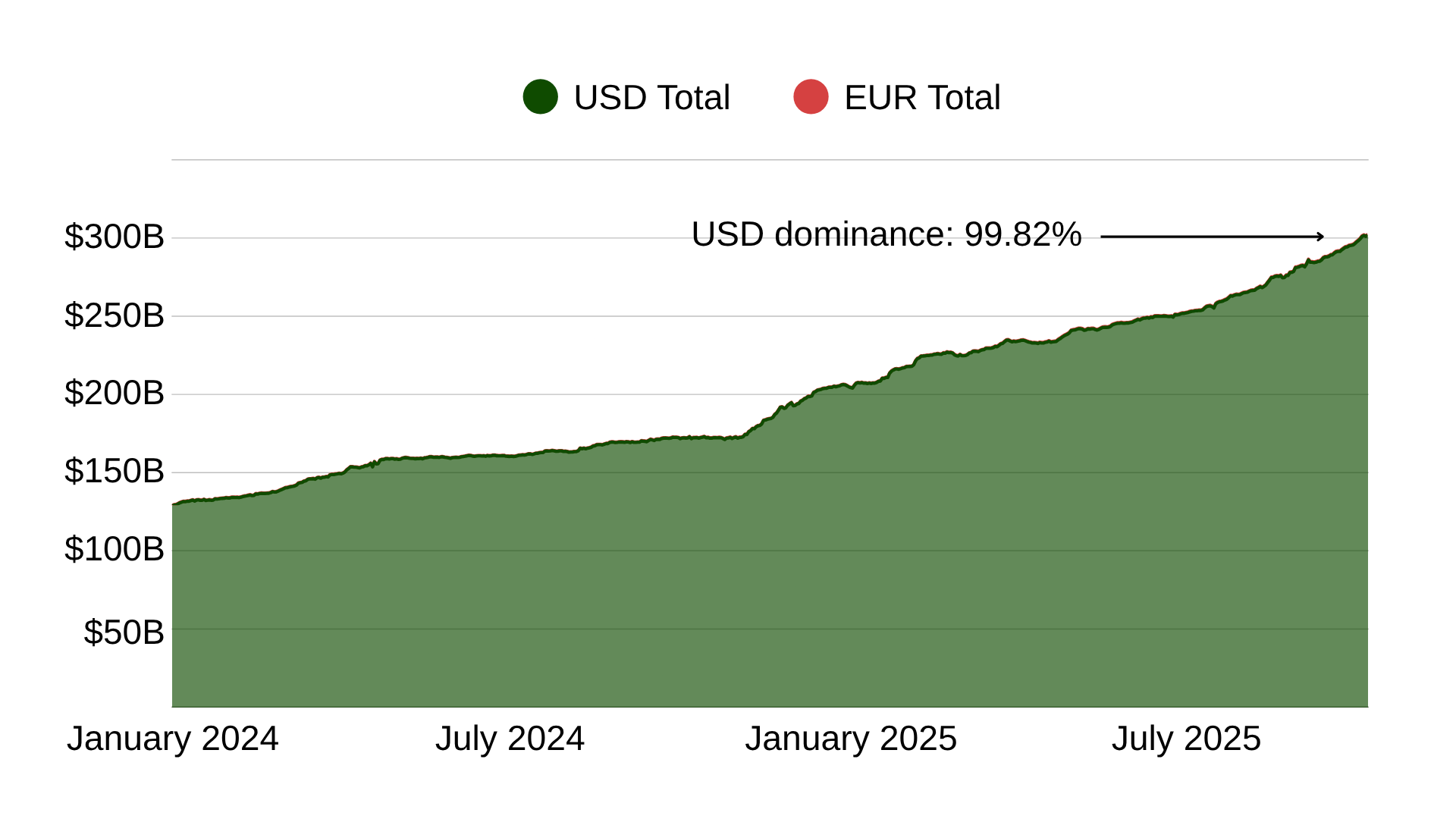

Whether the consortium model – and the stronger network effects it promises – will help them reach their goals remains to be seen. Still, it’s encouraging to see European institutions taking the “stablecoin race” seriously and working to bring the euro into the digital realm, which so far has been almost entirely dominated by the U.S. dollar.

Societe Generale Pushes EUR Stablecoin into DeFi

Other institutions, meanwhile, are already making significant moves in DeFi.

Societe Generale, through its blockchain arm SG-FORGE, has become the first global systemically important bank to integrate its stablecoins (EURCV and USDCV) into permissionless DeFi protocols.

First, users can now lend and borrow EURCV on Morpho, one of the leading decentralized lending protocols. These loans are overcollateralized, meaning users deposit assets like ETH, BTC, or tokenized money market funds to borrow against.

One of those collateral options is a tokenized money market fund issued by Spiko, a Blockwall portfolio company.

Second, SG-Forge has launched trading pools for EURCV on Uniswap, allowing anyone to buy or sell the stablecoin in a fully decentralized, permissionless manner.

Obviously, these integrations are designed to boost the availability and usability of EURCV across crypto-native environments.

And the move has other major implications. If a Tier-1 bank can successfully operate within DeFi frameworks while meeting regulatory standards, others are likely to follow – and they will. DeFi, after all, has proven to be one of the strongest catalysts for stablecoin adoption.

DeFi protocol Ethena offers a clear example. Through deep integrations with lending platforms such as Aave, their synthetic dollar, USDe, has grown its circulating supply to nearly $14 billion in under two years, making it the third-largest USD stablecoin in record time.

PayPal, too, understands the power of DeFi incentives. The company currently distributes around $70,000 in additional rewards to users who hold its PYUSD stablecoin in DeFi protocols – a campaign that has coincided with a sharp rise in PYUSD supply.

But while incentives can attract liquidity, keeping it is far more difficult. Real utility is what makes liquidity “stick.” For banks and corporates, this means having a clear vision of what their stablecoin is meant to achieve before launching costly incentive programs. Otherwise, those efforts risk becoming expensive experiments.

How (Europe’s) new entrants navigate this new terrain will be fascinating to watch.

SEC Streamlines Crypto ETF Approvals

For the last major announcement in September, we look over the Atlantic to the U.S.

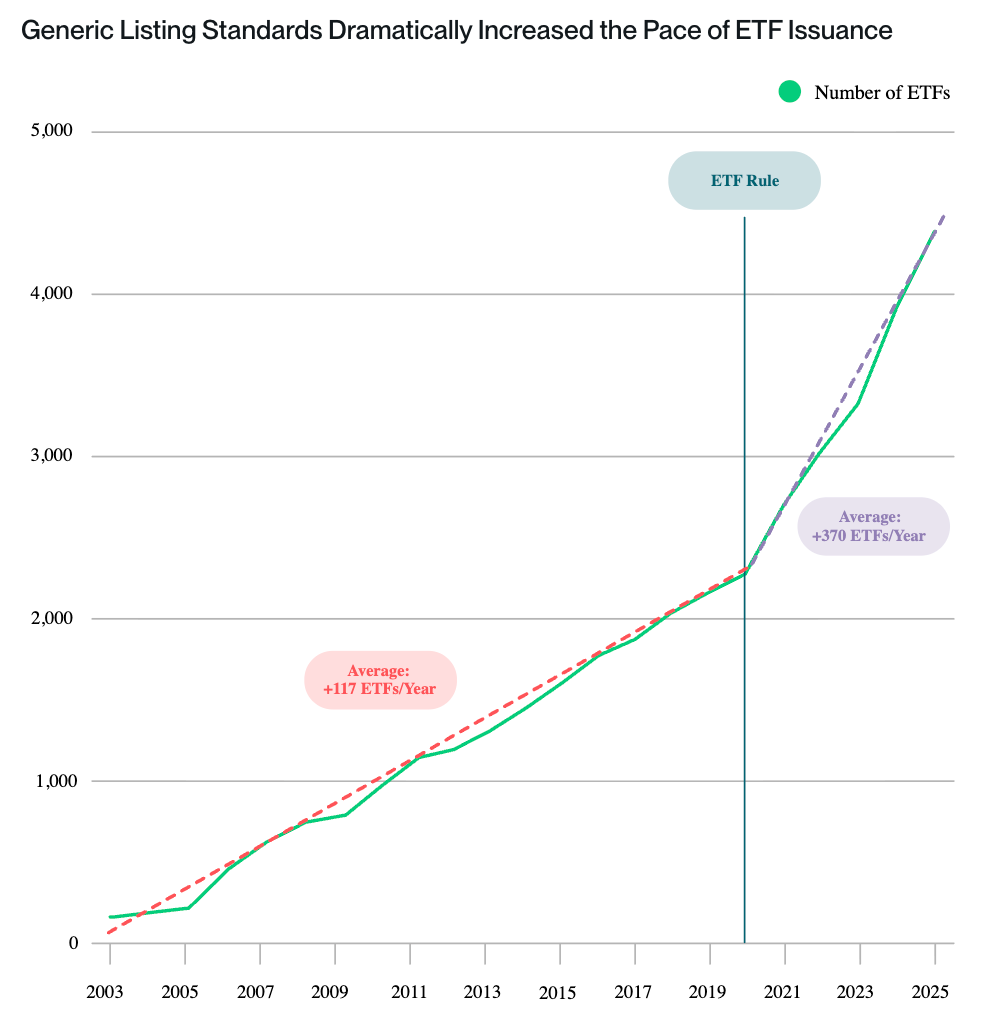

There, the SEC approved a new fast-track approval process for digital asset ETFs. Under the updated rules, exchanges such as Cboe, Nasdaq, and NYSE can now list spot crypto ETFs that meet standardized requirements without needing individual green lights from the regulator.

Concretely, this means that not all ETFs require the previously standard 240-day review cycle. Now, qualifying products can move to market in a matter of weeks.

According to Galaxy Research, 11 crypto assets, including SOL, DOT, DOGE, and XRP, currently meet the criteria, and just days after the rule change, we already saw spot ETFs launched for assets like DOGE and XRP, kicking off what many expect to be a wave of launches.

Now, what impact can we expect? Bitwise CIO Matt Hougan offered some helpful historical context: when the SEC introduced the generic listing standards for traditional ETFs in 2019, the average number of new launches tripled. He expects crypto to follow a similar trajectory, evolving from just a handful of flagship products to a much broader market.

Beyond that, Hougan anticipates a rise not only in single-asset ETFs but also in index-based products that track a basket of digital assets, making diversified exposure easier for investors.

According to Hougan, this expansion matters because a broader product landscape attracts more traditional investors and leads to deeper allocations. Crypto allocations that today represent 0.5% or 1% of institutional portfolios could grow meaningfully as more specialized and diversified products come to market.

Key Events of the Last Few Weeks

- Openbank launches cryptocurrency trading in Germany. Santander’s digital banking arm has rolled out crypto trading for retail customers, allowing users to buy, sell, and hold digital assets like Bitcoin and Ethereum alongside traditional investments in a unified platform. (Source: Santander)

- BlackRock explores ETF tokenization. The world’s largest asset manager is working on turning ETFs, particularly those backed by real-world assets like stocks, into blockchain-based tokens. (Source: Bloomberg)

- Morgan Stanley issues crypto allocation guidance. For the first time, the bank’s Global Investment Committee has recommended Bitcoin exposure via spot ETFs, with suggested allocations of 2 to 4% depending on portfolio strategy. The guidance supports 16,000 advisors managing $2 trillion in assets. (Source: X)

- Stripe introduces stablecoin issuing platform. The payments giant has launched “Open Issuance,” a platform that lets businesses issue their own stablecoins, while Stripe handles reserves, liquidity, and compliance behind the scenes. Early adopters include major crypto players Phantom and Metamask. (Source: Stripe)

- CME Group to launch 24/7 crypto futures and options trading. The world’s largest derivatives exchange plans to offer round-the-clock crypto trading in early 2026, pending regulatory approval. (Source: CME Group)

- Coinbase launches stablecoin lending inside its app. Users can now lend USDC directly within the Coinbase app, earning yields of up to 10%. The feature is powered by DeFi protocol Morpho and further integrates decentralized finance into mainstream user experiences. (Source: Coinbase)

- Brex to enable stablecoin payments for 20,000 businesses. The leading spend management platform is rolling out USDC payment functionality on Solana. This allows customers to send and receive stablecoins for faster, low-cost settlement. (Source: Brex)

What We’ve Been Reading

- Stablecoins 2030 (Citi) — A forward-looking report exploring how stablecoins could reshape payments, banking, and capital markets by 2030. Covers adoption drivers, regulatory frameworks, reserve models, technical architecture, and the competitive landscape between private and public digital money initiatives.

- What Is a Stablecoin? (McKinsey) — An explainer on the mechanics, risks, regulation, and institutional impact of stablecoins as they become core to the digital money ecosystem.

- The Compelling Case for Crypto (Franklin Templeton) — An eight-part investor memo outlining why digital assets are becoming a strategic asset class. Topics include portfolio diversification, institutional adoption, blockchain-driven business models, shifting U.S. regulation, generational wealth trends, and the role of ETPs in making crypto more accessible.

Disclaimer

To avoid any misinterpretation, nothing in this blog should be considered as an offer to sell or a solicitation of interest to purchase any securities advised by Blockwall, its affiliates or its representatives. Under no circumstances should anything herein be interpreted as fund marketing materials for prospective investors considering an investment in any Blockwall fund. None of the data and information constitutes general or personalized investment advice and only represents the personal opinion of the author. The author and/or Blockwall may directly or indirectly be exposed to the mentioned assets/investments. For further information please view the full Disclaimer by clicking the button below.

This work is licensed under the Creative Commons Attribution – No Derivatives 4.0 International License. CC BY-ND 4.0 Legal Code | Creative Commons