Dear Founders, Investors, and Friends,

It’s great to have you back for the October 2025 edition of Blockwall Insights. Here’s what we’re covering today:

- Market Structure Stress Test: The October 10th Crash

- Fintechs are Coming for U.S. Banks

- Convergence: Crypto and Traditional Finance Draw Closer

- Galaxy Launches GalaxyOne

- Hyperliquid Brings U.S. Equities Futures Onchain

- Coinbase Builds the Onchain Capital Markets Stack

- Enterprise Adoption: IBM and Oracle Move into Digital Assets

- Blockwall Company Update

- Key Events of the Last Weeks

- What We’ve Been Reading

Executive Summary

October delivered a defining stress test for global crypto markets. A late-day geopolitical shock triggered the largest selloff in the industry’s history, erasing more than $600 billion and forcing a rapid deleveraging cycle. Centralized venues faltered under pressure, while decentralized systems processed record liquidations without failures, reinforcing the shift of trust, liquidity, and trading activity toward transparent onchain infrastructure.

Regulatory and competitive dynamics in the U.S. financial system accelerated. A surge of fintechs and crypto firms applied for national trust bank charters, positioning themselves to handle payments, custody, and stablecoin issuance directly. Regulators signaled readiness to approve these new digitally native institutions, setting up direct competition with incumbent banks.

The broader convergence of crypto and traditional finance advanced through three major moves: Galaxy’s retail expansion with GalaxyOne, Hyperliquid’s introduction of perpetual markets for traditional assets, and Coinbase’s acquisition of Echo to unify the full lifecycle of onchain capital formation. Each development brings traditional instruments closer to programmable, global market infrastructure.

Enterprise adoption strengthened as IBM and Oracle introduced institutional digital asset platforms that integrate custody, settlement, and tokenization into existing financial systems, pushing the technology into mainstream capital markets.

For Blockwall, the successful first closing of Blockwall Capital III and the momentum at our Investor Summit reflect a market that has matured into real deployment. Portfolio highlights from Spiko and Tranched underline the pace at which the ecosystem is professionalizing. The direction is clear: financial markets are consolidating around open, resilient, and programmable infrastructure.

s

This month, the crypto market witnessed its largest selloff ever, surpassing previous crashes like the 2021 flash crash and the FTX collapse. It erased over $600 billion (roughly 15%) of crypto’s total market capitalization, with a record-breaking $20 billion in positions liquidated across 1.6 million individual accounts.

While the trigger was a tweet by U.S. President Donald Trump threatening new tariffs on China, two structural dynamics amplified the shock.

First, the timing. Trump’s tariff announcement hit after U.S. markets had closed, leaving crypto as the only major asset class still trading. With no ETF inflows or traditional liquidity available to offset the move, the full repricing occurred within crypto venues.

Second, leverage in the markets had quietly reached record levels. As the first liquidations began, they cascaded through the system, wiping out open interest by over 60% and sending many assets down 70-90% within seconds.

This is where the difference between centralized and decentralized market resilience became obvious:

- As volatility spiked, market makers withdrew from order books, exposing the lack of natural bids in long-tail assets.

- Binance, the world’s largest centralized exchange, experienced an hour-long outage.

- Major exchanges triggered widespread Auto-Deleveraging (ADL) events, forcibly closing even profitable positions to remain solvent. For many traders, this move came as a surprise and revealed just how little transparency exists around these

mechanisms.

DeFi applications, on the other hand, handled the stress test far better, with all mechanisms working as intended:

- Lending platforms like Aave and Morpho processed record liquidations without incurring any losses for their users.

- Hyperliquid, the industry’s largest decentralized derivatives trading venue, stayed fully operational throughout the crash.

- Ethena, the platform behind the largest decentralized synthetic dollar, USDe, handled billion-dollar redemptions with only a minor deviation from its dollar peg.

This is also why, after the crash, researchers observed a rise in onchain trading volumes and a capital rotation toward blockchain-based applications.

Combined with the broader trend of trading volumes migrating onchain throughout the year, the message is clear: trust and liquidity are moving to permissionless and transparent infrastructure that scales under pressure.

When it comes to the broader market, it failed to recover meaningfully, with uncertainty and fear still dominating sentiment. Whether an end to the U.S. government shutdown and greater clarity on trade policy will stabilize markets remains to be seen.

Fintechs are Coming for U.S. Banks

October also intensified the competition between fintechs, crypto firms, and traditional banks. Within weeks, several major fintech and crypto players applied for national trust bank charters from the U.S. Office of the Comptroller of the Currency (OCC). Stripe’s stablecoin subsidiary Bridge, Sony Bank’s Connectia Trust, and Peter Thiel-backed Erebor Bank all joined the list. They follow earlier applicants including Circle, BitGo, Ripple, Paxos, and Coinbase.

Now, why are they doing this? Since the passage of the GENIUS Act in July, the OCC charter has become the key regulatory pathway for firms aiming to merge payments, custody, and stablecoin issuance. It offers three main advantages: a single federal oversight regime, legal custody of stablecoin reserves, and eligibility for a Federal Reserve master account, allowing direct Fedwire access and near-instant settlement without relying on commercial banks.

In short, this means entities holding this charter can hold and move money independently of traditional intermediaries. It will make them compete directly with banks for deposits and payments, creating a new class of digitally native institutions that merge custody, settlement, and payments within a single stack. This ultimately changes and challenges the notion of what a “bank” can be.

This is an especially pressing question for incumbent banks. And while they were able to shield themselves from similar disruptions in the past through regulatory intervention (as seen with Meta’s Libra initiative), this time regulators appear more open to change. The relatively fast preliminary approval for Erebor Bank by the OCC illustrates that shift.

If the outstanding charters are granted in the coming months as well, traditional banks will need to adapt quickly to a new competitive reality.

Convergence: Crypto and Traditional Finance Draw Closer

Meanwhile, crypto-native firms already pushed further into traditional finance. In that regard, three announcement especially stood out: Galaxy Digital’s launch of GalaxyOne, Hyperliquid’s expansion in equity and commodity derivatives, and Coinbase’s acquisition of onchain fundraising platform Echo.

Galaxy launches GalaxyOne

Historically focused on institutional trading, lending, and asset management, Galaxy is now expanding into the retail market. With GalaxyOne, the company aims to bring traditional and crypto asset trading, investing, and yield generation together under one platform.

The move leverages Galaxy’s existing institutional lending operations. Customer deposits are used to fund professional-grade loans, enabling depositors to earn up to 8% APY. In essence, Galaxy is repackaging institutional infrastructure for a retail audience, offering the same systems and credit relationships that previously served only funds and corporates.

This strategy carries broader implications for the market. By channeling traditional capital onto onchain rails, Galaxy is helping integrate conventional financial flows with decentralized infrastructure. As liquidity in DeFi deepens and becomes less scarce, rates are likely to compress, making the ecosystem more efficient and appealing to professional allocators. It marks another step toward a more mature, interconnected market where crypto and traditional finance no longer operate in isolation.

Hyperliquid Brings U.S. Equity Futures Onchain

Hyperliquid, crypto’s leading decentralized derivatives platform, made a major push toward integrating traditional assets. Its latest upgrade enables the creation of perpetual markets, meaning futures contracts without an expiry date, for any asset class, including commodities and U.S. equities such as Tesla and Nvidia.

While initial traction on the first market that allows traders to speculate on the Nasdaq remained moderate, with open interest accounting for roughly 0.8% of Hyperliquid’s total, and creating these markets still relatively complex and costly for users, the move is nonetheless significant.

It gives anyone with a smartphone and an internet connection direct price exposure to U.S. capital markets, a major step toward more open and inclusive global finance. It also marks Hyperliquid’s expansion beyond crypto derivatives and toward a universal trading layer where all assets can exist side by side. This shows how financial markets are gradually merging into shared, programmable infrastructure that allows participants to trade both crypto and traditional instruments under the same ruleset.

Coinbase Builds the Onchain Capital Markets Stack

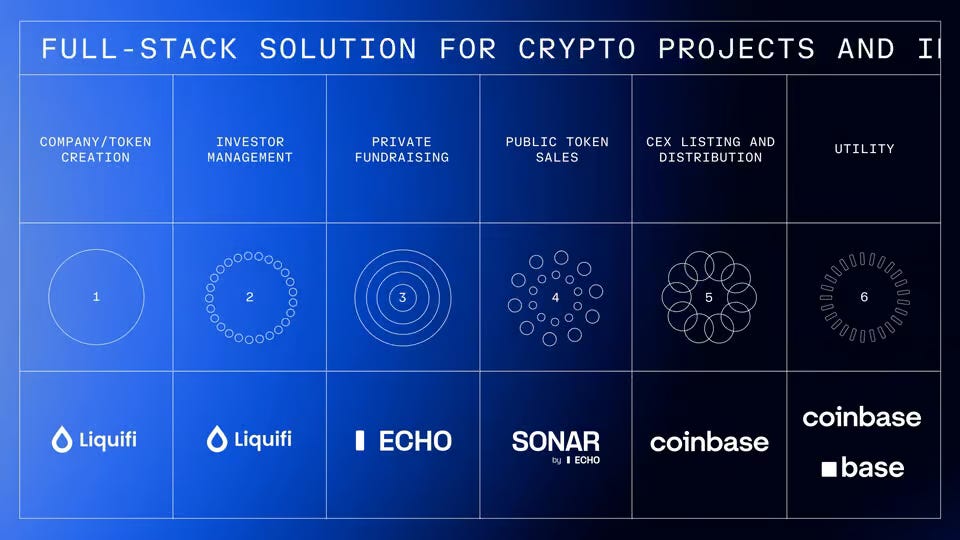

The last and most significant announcement in October highlighting the convergence between traditional and onchain finance was Coinbase’s $375 million acquisition of Echo, the leading onchain fundraising platform.

While some may question such a high price tag for a platform that has likely generated limited revenue so far, the strategic value for Coinbase is substantial. Combined with the firm’s existing infrastructure, Echo enables Coinbase to cover the entire lifecycle of digital assets onchain:

- Issuance: Echo, facilitating compliant onchain fundraising

- Token management: Liquifi, the platform Coinbase acquired earlier this year

- Secondary trading: Coinbase’s centralized exchange

- Decentralized trading and DeFi integration: Base, Coinbase’s Layer 2 network

Together, these components create a comprehensive, end-to-end infrastructure for both primary and secondary markets, positioning Coinbase as a central hub for onchain capital formation.

The acquisition also lays the groundwork for expansion beyond crypto tokens. Coinbase has already indicated plans to extend these capabilities to tokenized securities and real-world assets once regulatory clarity allows.

Taken together, all these moves show the direction of travel. Crypto firms are no longer building parallel systems; they are integrating with traditional markets, adopting familiar instruments, and reengineering financial infrastructure from the ground up. The lines between fintech, crypto, and traditional finance are blurring, and the resulting market will be unified, not divided, by technology.

Enterprise Adoption: IBM and Oracle Move Into Digital Assets

Finally, October saw major enterprise technology providers enter digital asset infrastructure. IBM launched Digital Asset Haven, a platform for institutions to custody, manage, and settle tokenized assets. Built with wallet provider Dfns, Haven integrates IBM’s mainframe security stack with crypto-native wallet capabilities, enabling clients to interact with exchanges and DeFi protocols through a single interface.

IBM’s positioning is strategic. The company already runs the backbone of global payment and capital markets systems. Extending that reliability to digital assets gives institutions a path to tokenization without migrating to external providers. Haven’s launch will start with a cloud-based service this year, followed by on-premise deployment for regulated banks in 2026.

Oracle followed with its own announcement of Digital Asset Data Nexus, a platform set to launch in 2026 supporting both permissioned and public blockchains. Like IBM’s initiative, it targets financial institutions seeking to issue and transact digital assets natively within their existing environments.

Now, with these moves, tokenization is advancing into institutional finance not only from the outside but also from within the existing system, accelerating its integration into global markets.

Blockwall Company Update

Reflections on Blockwall’s 3rd Investor Summit

Another fantastic Blockwall Investor Summit is in the books. This time, we were also pleased to announce a major milestone:

The first closing of our new fund, Blockwall Capital III.

This fund builds on the insights and track record of Fund I and Fund II, with a holistic focus on pre-seed and seed investments in the Web3 space.

And as the panels at our Summit have once again shown, the timing just couldn’t be better.

- Blockchain infrastructure is finally scalable

- Regulation has caught up through frameworks like MiCA in Europe and the Genius Act in the U.S.

- Large financial institutions such as BlackRock and Franklin Templeton, and major fintechs like Stripe and Robinhood, are all participating in the market

- Stablecoins, tokenization, and onchain payments have become integral to corporate treasury and cash management, enabling instant, low-cost transfers and real liquidity

In short: the Web3 ecosystem has matured from experimentation to real adoption.

And it was truly inspiring to see these developments echoed across the conversations and panels at the Summit.

Thank you to all speakers for your valuable insights: Bert Staufenbiel, Ivan de Lastours, Christoph Hock, Torsten Hunke, Manfred Knof, Mathias Imbach, Yat Siu, Paul-Adrien Hyppolite, Michael Duttlinger, Hendrik König, Dorothea Ysenburg, Alexander Hoeptner, Casper Yonel, Christopher Beck, Gaia Ferrero Regis, Steven Figura, Romain Schneider, Axel Cateland, and Arjun Sethi.

And thank you to everyone from the Blockwall team who made this possible: Jannis Choulidis, Nikos Choulidis, Damien Roch, Max Schneider, Syed Armani, Leonard Lang, Havard Rivedal, Bjarmi Leo and Lars Singbartl.

For anyone who couldn’t attend: Over the coming days, weeks, and months, we’ll be sharing more content, highlights, and the full recording of the Summit with you. To stay in the loop, feel free to follow our Blockwall account on LinkedIn.

Celebrating Tranched and Spiko

This month, two of our French portfolio companies had reason to celebrate.

First, Spiko was named Startup of the Year at AMTechDay, one of Europe’s premier conferences showcasing innovation in the asset management industry. In addition, its onchain treasury products have surpassed €500 million in assets under management. Congratulations, Antoine and Paul-Adrien!

Second, Tranched was selected as part of the Future 40 2025, STATION F’s annual list recognizing the 40 best-performing startups on campus – representing just 4% of the 1,000+ companies there. Very well done, Michaël and Clément!

Key Events of the Last Few Weeks

- Luxembourg proposes Bitcoin allocation. The country’s Intergenerational Sovereign Wealth Fund (FSIL) plans to allocate 1% of its portfolio, around $7 million, to Bitcoin through ETFs, according to the finance minister. This would make Luxembourg the first Eurozone country whose sovereign wealth fund adopts a strategic allocation to digital assets. (Source: Luxembourg Times)

- Major players receive MiCA licenses. Fintech giant Revolut, crypto platform Blockchain.com, and Bitcoin app Relai can now offer their crypto services across the European Economic Area. (Source: LinkedIn)

- Bitwise debuts BSOL ETF. The first-ever staked spot SOL ETF in the U.S. recorded $56 million in first-day trading volume, making it the highest-volume ETF launch of the year. (Source: Bitwise)

- More crypto IPOs on the way. Tokenization platform Securitize filed to go public through a SPAC merger valued at $1.25 billion. Further, Axios reported that MetaMask creator Consensys had selected JPMorgan and Goldman Sachs as lead underwriters for its upcoming IPO. (Sources: Securitize, Axios)

- FCA lifts retail ban on crypto ETNs. The UK regulator now allows retail investors to access crypto exchange-traded notes (cETNs) provided they are listed on an FCA-recognized exchange and have approved prospectuses. (Source: LinkedIn)

- DekaBank expands crypto trading to retail clients. Previously limited to institutional investors, the service will now reach retail clients through Boerse Stuttgart Digital. DekaBank is one of Germany’s largest asset managers, overseeing more than €400 billion in assets. (Source: Boerse Stuttgart Group)

- Morgan Stanley lifts crypto fund restrictions. The bank informed advisors that crypto investments are now open to all clients across all account types, including retirement accounts. This change affects 16,000 advisors managing $2 trillion in wealth. (Source: CNBC)

- Ten major banks form new stablecoin consortium. Santander, BNP Paribas, Bank of America, UBS, Deutsche Bank, Citi, and others are joining forces to explore issuing a 1:1 reserve-backed digital currency on public blockchains, initially focused on G7 currencies. The announcement follows ING, UniCredit, and DekaBank’s euro stablecoin initiative planned for 2026. (Source: BNP Paribas)

- JPMorgan to accept Bitcoin and Ether as collateral. After previously allowing only ETP-based loans, the bank will now accept spot BTC and ETH as collateral for institutional clients before year-end, signaling a deeper integration of crypto assets into traditional financing. (Source: Bloomberg)

What We’ve Been Reading

- Stablecoin Payments from the Ground Up (Artemis) — A data-driven study of how stablecoins are reshaping global payments, from consumer transactions to corporate treasury. The report maps real-world adoption, settlement volumes, and regional usage patterns, offering a granular look at how stablecoins are evolving into a core financial infrastructure layer. For the core insights, see Dominic’s LinkedIn post.

- State of Crypto 2025 (a16z) — An annual deep dive into the crypto ecosystem, analyzing key industry metrics across infrastructure, DeFi, consumer apps, and regulation. The report highlights the rise of onchain finance, developer activity trends, and how crypto adoption is shifting toward utility-driven use cases. For the core insights, see Dominic’s LinkedIn post.

- Digital Digest (State Street) — A quarterly publication exploring how tokenization, AI, and digital finance are reshaping institutional markets. This edition focuses on operational readiness, regulatory alignment, and how large asset managers are preparing for the transition to a tokenized financial system. For the core insights, see Dominic’s LinkedIn post.

Disclaimer

To avoid any misinterpretation, nothing in this blog should be considered as an offer to sell or a solicitation of interest to purchase any securities advised by Blockwall, its affiliates or its representatives. Under no circumstances should anything herein be interpreted as fund marketing materials for prospective investors considering an investment in any Blockwall fund. None of the data and information constitutes general or personalized investment advice and only represents the personal opinion of the author. The author and/or Blockwall may directly or indirectly be exposed to the mentioned assets/investments. For further information please view the full Disclaimer by clicking the button below.

This work is licensed under the Creative Commons Attribution – No Derivatives 4.0 International License. CC BY-ND 4.0 Legal Code | Creative Commons