Dear Founders, Investors, and Friends,

July marked a turning point for U.S. crypto regulation, with the GENIUS Act becoming law and the CLARITY Act clearing the U.S. House. Meanwhile, tokenized stocks took center stage, and digital asset treasury companies poured billions into the market, helping drive BTC to new all-time highs and sparking a broader resurgence in altcoins — most notably ETH.

So, without further ado, let's unpack the month’s most important developments.

U.S. Crypto Regulation: GENIUS Becomes Law

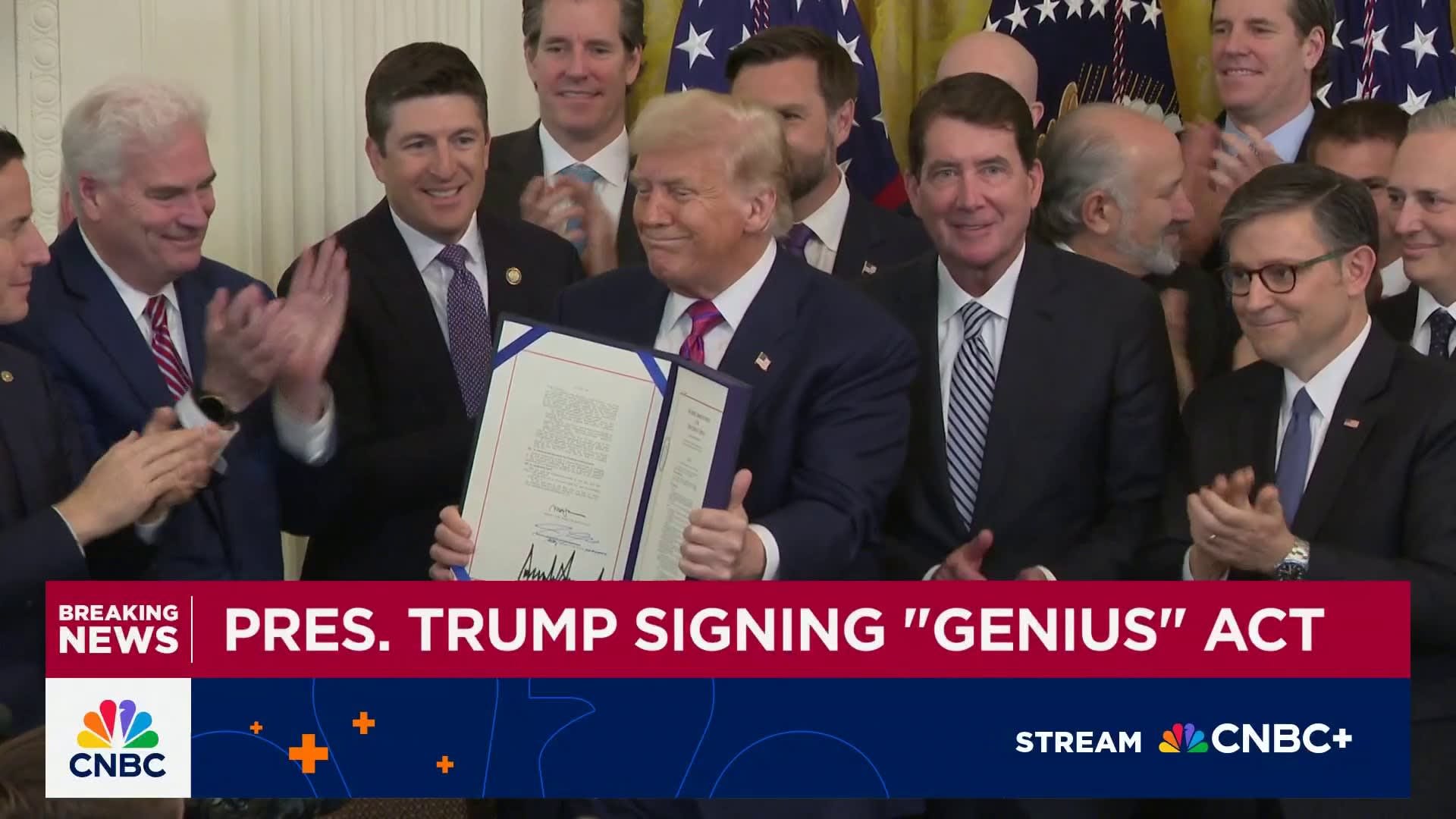

This is what the industry has been waiting for. On July 17th, the U.S. House passed the GENIUS Act with a supermajority of 308–122. Just one day later, President Trump signed it into law.

The GENIUS Act introduces the first U.S. federal framework for payment stablecoins, with key provisions including:

- Full reserve backing: 1:1 backing with cash, U.S. Treasuries, or repurchase agreements, held in segregated accounts at U.S. banks or regulated institutions

- Federal registration: Issuers must register with the Federal Reserve or OCC, with larger issuers ($10B+ circulation) falling under direct federal oversight

- Tiered regulation: Smaller issuers (under $10B) may operate under qualifying state regimes instead of federal oversight

- Regular reporting: Monthly, independently audited reports on reserve composition and financial health

- No yield sharing: Stablecoin issuers are prohibited from paying interest directly to users, keeping stablecoins in the payments lane rather than competing with bank deposits

- Corporate restrictions: Commercial companies face antitrust checks and must create separate entities to issue stablecoins (the "Libra clause")"

In short: the green light is on. Banks, fintechs, and infrastructure providers now have the clarity to turn pilot programs and announcements from the recent months into products. Expect the stablecoin landscape in the U.S. to evolve quickly.

But beyond domestic adoption, the Act has far-reaching geopolitical implications. Because so much of the crypto economy already settles in stablecoins, anchoring reserves inside U.S. financial institutions puts the regulation of a large part of the onchain economy within U.S. jurisdiction. This could serve as a powerful strategic lever in the years ahead.

The bigger picture? The U.S. is offering a regulatory framework the industry is eager to work within; a move that potentially intensifies the battle for talent and crypto innovation between the U.S., Europe, and the rest of the world.

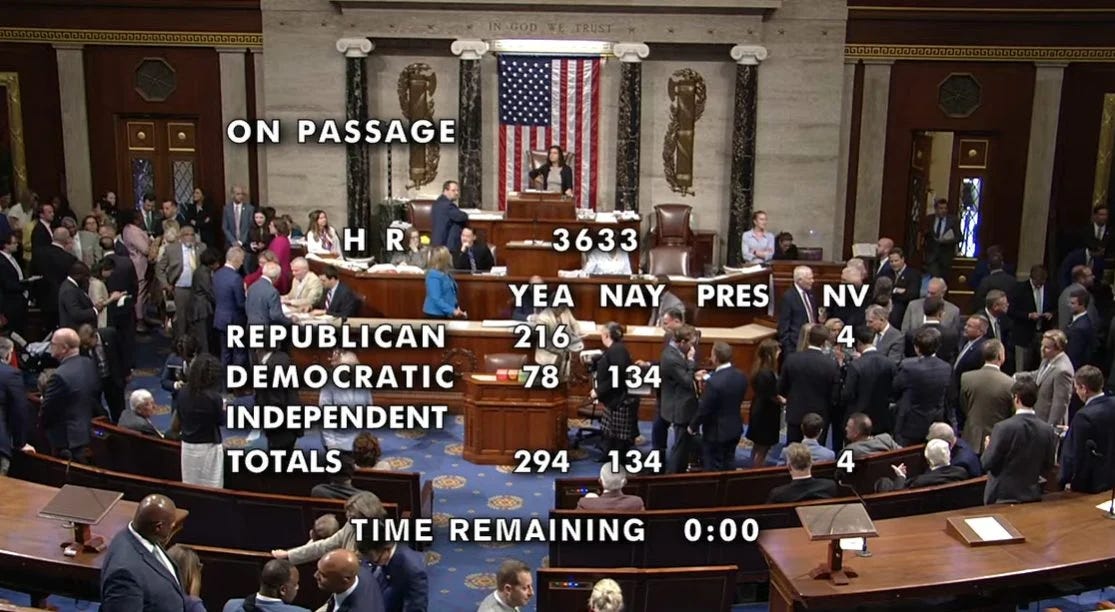

Crypto Market Structure Bill Clears U.S. House

The same day GENIUS was passed, lawmakers advanced a second major piece of legislation. The CLARITY Act passed the House with a 294–134 vote and is now being discussed in the Senate.

CLARITY is the first comprehensive crypto market structure bill designed to regulate the digital assets industry, addressing a long-standing question: Which digital assets qualify as securities, and which fall under the category of commodities?

Under CLARITY, blockchain-native assets with functional utility and decentralized control would be regulated by the CFTC as "digital commodities." In contrast, assets tied to centralized issuers or resembling investment contracts would remain under SEC oversight.

Another key aspect is how the bill incorporates decentralization as a regulatory dividing line. Entities that directly manage or custody user funds — such as centralized exchanges or custodians — will face more stringent requirements. But actors including wallet providers, validators, frontend developers, and app teams that do not touch user funds, could qualify for tailored exemptions and lighter-touch regulation.

Similar to the EU's MiCA, CLARITY is designed to give the U.S. a competitive edge by creating an environment where Web3 developers and digital asset companies can operate with more certainty, bringing innovation back onshore. However, unlike MiCA's unified European framework and strict definition of different token types (E-Money tokens, Utility Tokens, Asset-referenced tokens), CLARITY introduces regulatory clarity by splitting responsibility between federal agencies, based on the technical and operational structure of projects and tokens. Time will tell which approach leads to better results.

But as of now, it's way too early for any predictions. The final form of the legislation may (and certainly will) change before it becomes law, and its ultimate impact will depend on how it's implemented. Still, the U.S. is signaling to the world that it intends to lead on digital asset regulation, offering a clear path forward where many jurisdictions still hesitate.

And the U.S. wants to move quickly, with key lawmakers having set a clear target: deliver a finalized market structure bill to the President’s desk by the end of September.

Tokenized Stocks Gain Significant Attention

Tokenized stocks took a major leap forward last month with both Kraken and Robinhood launching their offerings (on the same day).

While Kraken's xStocks offering initially features 55 tokenized U.S. stocks and 5 ETFs and is not officially available in major jurisdictions like the U.S., the EU, Australia, Canada, and the UK, Robinhood's offering includes a whopping 200 stocks and ETFs that are now available to eligible users, focusing on the EU.

However, the initial excitement around what this means for blockchain adoption was quickly tempered by some important questions about what these "tokenized stocks" actually deliver.

Kraken's xStocks are blockchain-based tokens backed 1:1 by actual shares held in custody by a regulated entity in Jersey. While these tokens can be self-custodied, traded onchain, and used in DeFi applications, holders don't have direct legal ownership of the underlying stocks. Instead, they hold tokens that track price performance without voting rights, dividend rights, or any claim to the company's assets.

Robinhood's approach is different but equally limited when it comes to voting rights and dividend claims. Their tokenized stocks are derivative contracts tracking U.S. stock prices, recorded onchain but operating within Robinhood Europe's closed ecosystem. This means: in contrast to Kraken, the tokens cannot leave the Robinhood platform and thus cannot be self-custodied — although Robinhood said that this will change in the months ahead.

Naturally, these limitations raised an obvious question: are we looking at genuine innovation here, or just a familiar product dressed up in shinier packaging?

While it's a fair critique given what's available today, we still need to keep in mind that this is really just the beginning of bringing equities onchain. Meanwhile, the broader momentum and potential impact is hard to ignore: For users in emerging markets dealing with limited brokerage access or currency instability, tokenized stocks, in their eventual full form, represent direct access to U.S. capital markets and a compelling tool for wealth creation and preservation.

Still, the key word there is "eventually." Right now, the regulatory pieces still need to fall into place so that token holders can actually get the same rights as traditional shareholders. But given how fast things are moving in Washington, that future doesn't feel very far away.

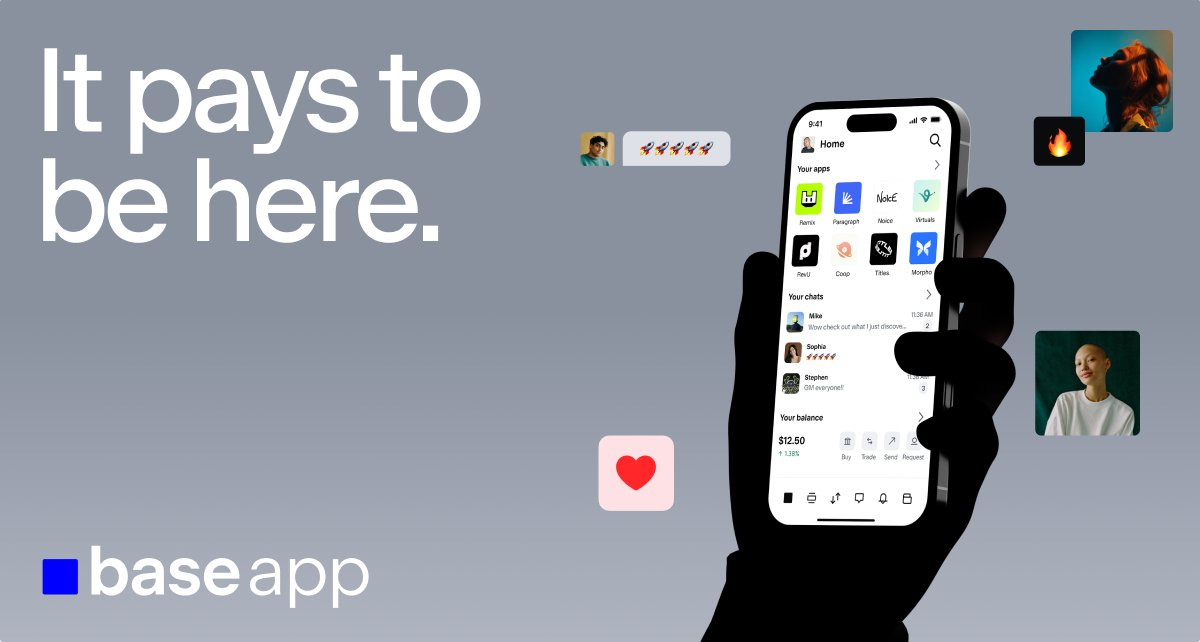

Coinbase Announces Push into Social

While everyone was announcing tokenized stock offerings, Coinbase made a bold move in a completely different direction: social.

The company unveiled an overhaul of its Coinbase Wallet (now the Base App) and a new suite of developer primitives, all aimed at accelerating adoption of its onchain ecosystem.

The centerpiece is the new Base App, which combines social feeds, payments, messaging, and trading into what CEO Brian Armstrong calls an "onchain super app." The app features a social feed powered by the social network protocol Farcaster, where every post is tokenized through the Zora protocol, allowing users to collect or trade posts as tokens directly within the feed.

Underlying this is the new Base Account system, which creates a portable onchain identity for users. Think of it as storing your name, email, and address onchain so you can carry that information across different applications. This also powers Coinbase's new "Sign in with Base" feature — essentially their version of "Sign in with Google" for the onchain world.

Further, the company is rolling out Base Pay, an express checkout system for USDC transactions on the Base Chain, which will be integrated into Shopify.

For Coinbase, this push represents an interesting strategic shift. Rather than just facilitating crypto trading and DeFi activity, the company is now seemingly betting on transforming its blockchain network into something like an app store and a platform where users can engage directly with onchain applications.

Considering the broader picture, one could see a rationale behind the move. The exchange's Base Chain is already Ethereum's most active Layer 2, and by broadening its focus beyond DeFi, it could attract more developers, apps, and users, thereby strengthening its lead, accelerating Base Chain's path to mainstream adoption, and generating revenues that substantially exceed what DeFi alone could produce.

However, the strategy carries significant risk. Social lies outside Coinbase's core competencies and Web3 social is a category that has yet to demonstrate clear product-market fit. Still, if executed well, the potential upside may well justify the risks.

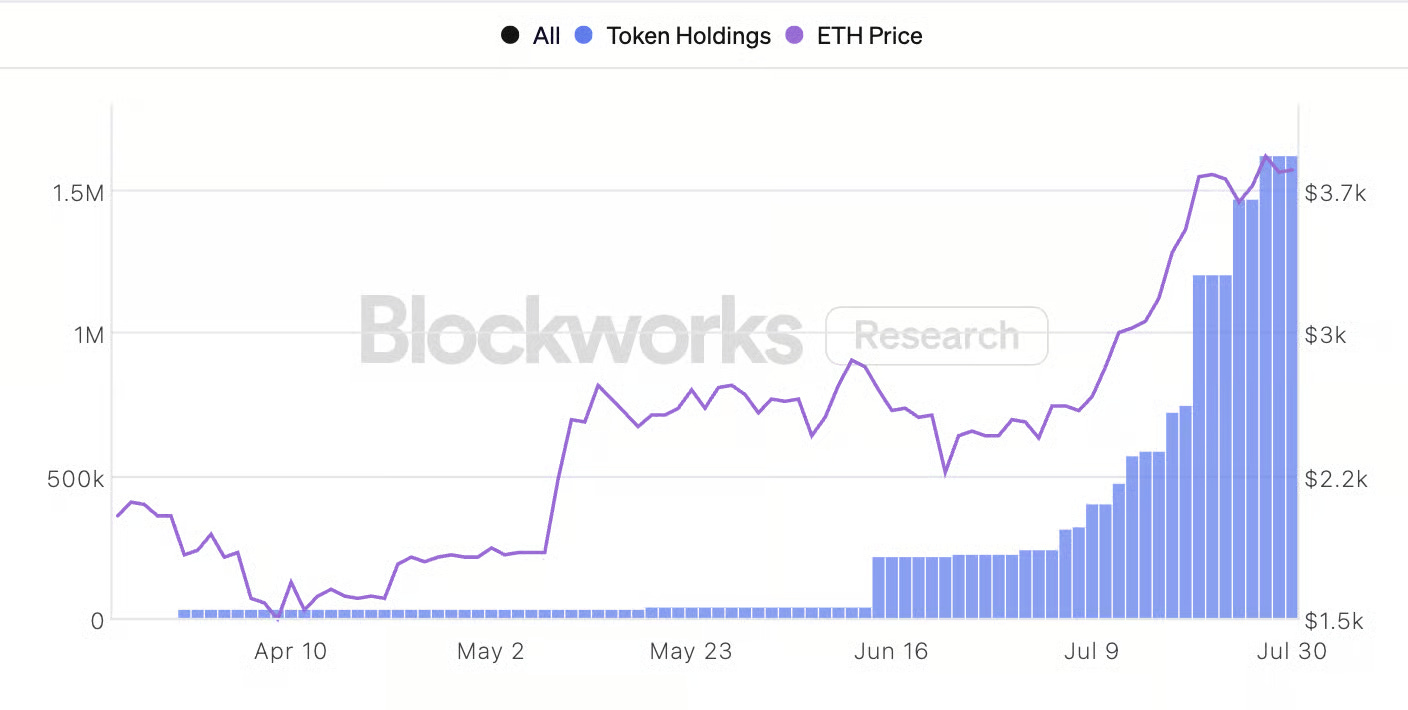

The Rise of Digital Asset Treasury Companies

July saw a notable acceleration in what has come to be known as the digital asset treasury model, which was pioneered by Michael Saylor and Strategy. At its core, the concept is simple: public companies raise capital (e.g. through issuance of their own stocks or debt) to acquire crypto assets.

Now, unlike traditional Bitcoin treasuries like Strategy, which only hold BTC as "digital gold," newly emerging vehicles are acquiring other assets and aim to actively manage their positions, targeting increases in tokens per share over time.

And the scale of these digital asset treasuries (DATs) is growing fast. Today, 38 publicly listed firms hold over $100 million in Bitcoin, while 5 companies have built comparable Ethereum positions. These ETH-based treasury companies, in particular, made headlines last month, acquiring approximately $6 billion in ETH, contributing meaningfully to Ethereum’s 55% price surge in July.

Whenever trends like this emerge, it’s worth zooming out. Put simply: these vehicles are financial engineering in its cleanest form. They do not deliver any meaningful fundamental value, nor do they create new access to crypto markets (despite frequent claims of democratizing exposure, the underlying assets are already widely accessible).

And while their impact has been undeniably positive for market prices in the short term, the longer-term effects are far more uncertain. Leverage is already creeping into some of these strategies. If conditions change, or if some of these firms signals intent (or are even forced) to sell part of their holdings to meet their debt obligations, markets could react sharply.

For liquid market participants, this is a trend worth monitoring closely. Because what looks like a tailwind today, could quickly become a risk factor tomorrow.

P.S. For those interested in a deeper dive into DATs, we've included a link to a podcast that covers the topic in more detail in our "What We've Been Reading" section down below.

Portfolio Update

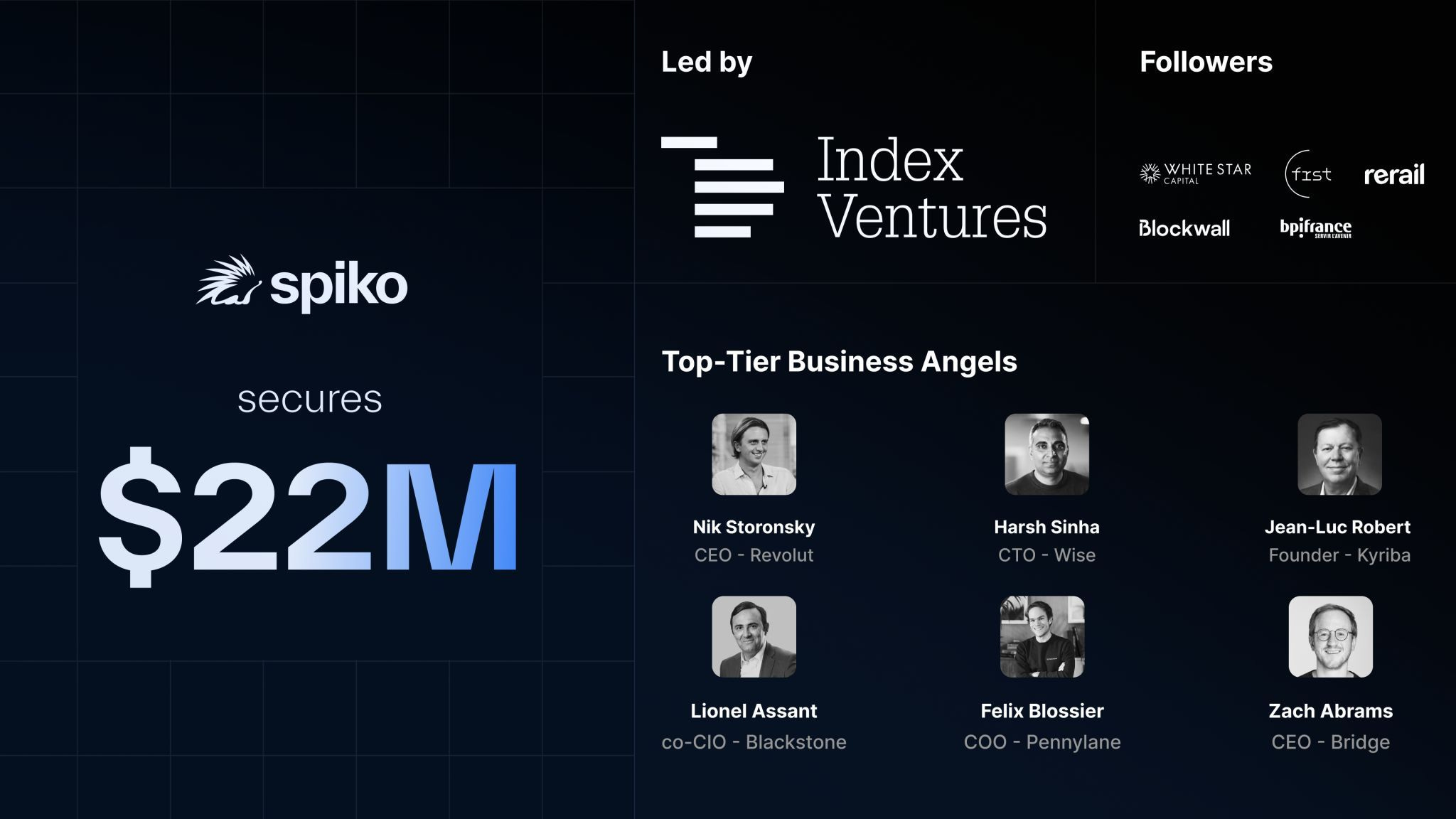

In July, one of our portfolio companies reached a major milestone: Spiko raised $22M for its Series A.

The round is led by Index Ventures, with participation from 199 Ventures, Athletico Ventures, Bpifrance's Digital Venture Fund, White Star Capital, Frst, Rerail, and ourselves at Blockwall.

After backing Spiko's pre-seed round, we doubled down by participating in this Series A.

Beyond that, the round saw participation from notable business angels including Revolut CEO Nik Storonsky, Wise CTO Harsh Sinha, Kyriba founder Jean-Luc Robert, Bridge co-founder Zach Abrams, Blackstone co-CIO Lionel Assant, and Pennylane's founding team (Arthur Waller, Felix Blossier, Tancrède Besnard).

Just one year after launch, Spiko has achieved $400 million in assets under management.

Beyond that, the team:

- launched Europe's first tokenized money market fund

- became the biggest issuer of tokenized treasuries on the Arbitrum layer-2

- is one of the top 10 biggest issuers of tokenized treasuries globally

It’s no stretch to say that projects like Spiko are the main drivers of crypto's institutional adoption.

They're building the infrastructure that brings real capital on blockchains, thereby fueling the growth of the "Onchain Economy".

And Spiko's success also carries broader implications for Europe.

Through their "Spiko Euro" product, they're accelerating adoption of EUR-linked investment products in a digital economy that remains 99% USD-dominated.

For more insights, please see Spiko’s blog post.

Congratulations Antoine and Paul-Adrien! Proud to support your journey from the beginning.

ICYMI: Blockwall Web3 Handbook

For everyone that missed it: Last month, we published the first version of our Web3 Handbook.

It offers a broad yet structured overview of the Web3 space — not from a purely technical or academic lens, but from the perspective of an active investor, innovator, or Web3-curious reader seeking to understand the foundational ideas shaping this ecosystem.

While long-form (~90 minutes read), it remains a high-level introduction. Feel free to read it end-to-end or dive into the sections most relevant to you. It does not aim to cover every aspect of Web3, but rather highlights the themes we believe are most important right now.

Key Events of the Last Few Weeks

- Banque de France develops onchain repo system on Ethereum. According to Blockstories, the current architecture behind the French central bank's protocol features a tokenized money market fund from our portfolio company Spiko. Full-scale testing is expected to begin before the end of 2025. (Source: Blockstories)

- JPMorgan is partnering with Coinbase. Starting this fall, Coinbase users will be able to pay with their Chase cards directly on the exchange. By 2026, they’ll also be able to link their bank accounts and convert credit card loyalty points into the USDC stablecoin on Base Chain. (Source: Coinbase)

- Another crypto company joins the S&P 500. Block, Jack Dorsey's Bitcoin-focused payments firm is now among the top 500 publicly traded companies in the U.S. (Source: Bloomberg)

- Germany's Sparkassen to offer crypto trading by mid-2026. Though the country's public savings banks don't plan on actively promoting or advising on crypto investments, they plan to offer access to regulated crypto assets via their Sparkasse app by next year. (Source: CoinDesk)

- BBVA launches crypto services for Spanish retail customers. The bank now offers Bitcoin and Ether trading and custody to all retail clients in Spain through its mobile app, alongside traditional banking products. (Source: BBVA)

What We’ve Been Reading

- The Crypto Treasury Playbook (Blockworks) — In this podcast, Ben Forman and Josh Solesbury from crypto VC ParaFi Capital dive deep into the details and current trends around publicly traded crypto vehicles.

- Blockchains as Emerging Economies (Fidelity Institutional) — In this report, Fidelity presents a novel framework called “digital GDP” to assess blockchains like Ethereum and Solana as standalone economies.

Disclaimer

To avoid any misinterpretation, nothing in this blog should be considered as an offer to sell or a solicitation of interest to purchase any securities advised by Blockwall, its affiliates or its representatives. Under no circumstances should anything herein be interpreted as fund marketing materials for prospective investors considering an investment in any Blockwall fund. None of the data and information constitutes general or personalized investment advice and only represents the personal opinion of the author. The author and/or Blockwall may directly or indirectly be exposed to the mentioned assets/investments. For further information please view the full Disclaimer by clicking the button below.

This work is licensed under the Creative Commons Attribution – No Derivatives 4.0 International License. CC BY-ND 4.0 Legal Code | Creative Commons