00

From keys to cards, bridging self-custody and everyday payments

When we wrote the first Blockwall thesis back in 2017, the core idea was simple: capital markets would gradually move on chain. Issuance, settlement and ownership would become software. Eight years later, that part is playing out fast. Tokenization is getting real, stablecoins have product-market fit, and institutional infrastructure has improved dramatically.

Yet one basic thing is still oddly hard: paying for everyday stuff directly from a wallet you control.

The size of the payments river

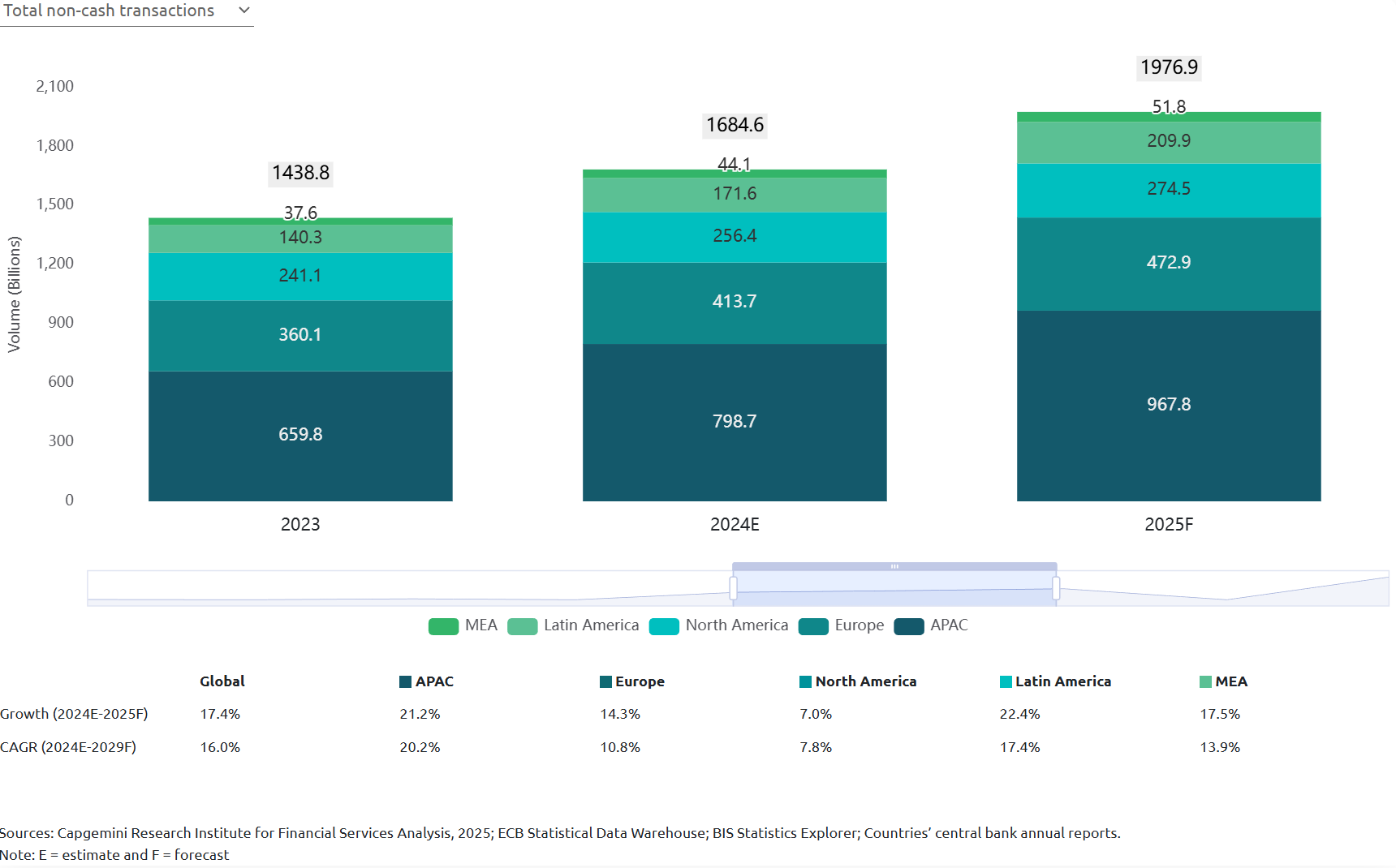

Global non-cash transactions have grown more than tenfold in less than twenty years, driven mainly by cards and account-to-account payments.

In the United States, card payments already make up roughly 63% of monthly consumer payments by number when you look at cash, cards and electronic transfers together. The euro area and the broader European Union look similar in pattern, even if the mix between cards and instant payments differs. Non-cash volumes are growing faster than GDP and cash’s share of point-of-sale transactions keeps falling.

On the consumer side, digital wallets are projected to account for about 61% of global e-commerce spending and 46% of point-of-sale spending by 2027, according to Worldpay’s Global Payments Report.

The conclusion is straightforward and well known: the main user interface for money in the traditional world is plastic or a phone screen linked to card and account rails so crypto has to find its way into spenders pocket to make it a valid payment use case.

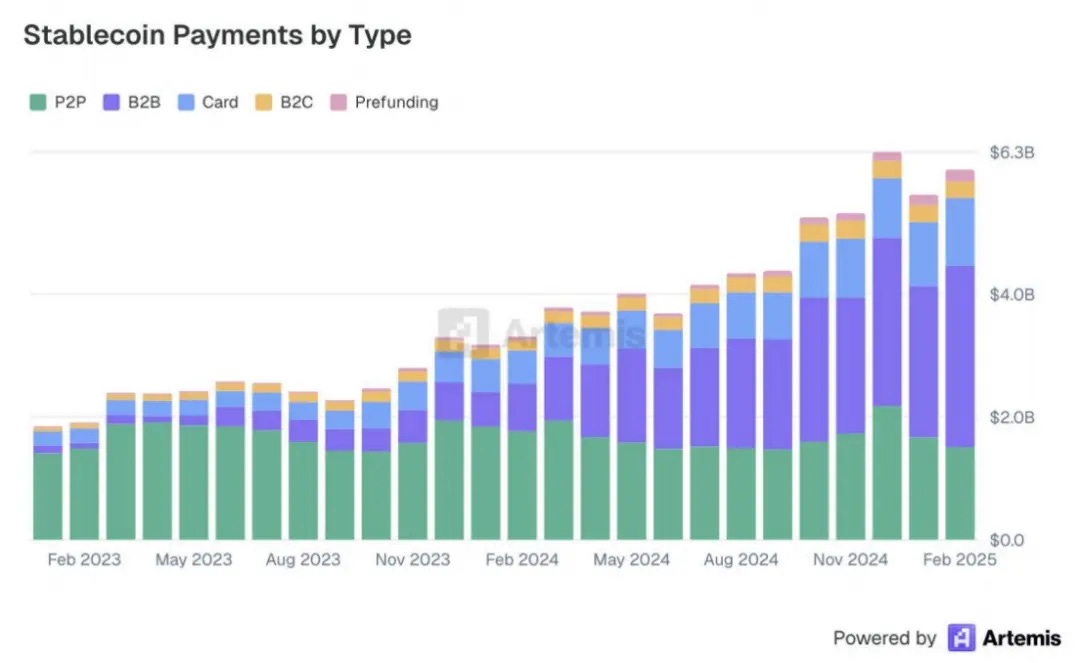

As a comparison it was estimated that monthly stablecoin payment volume through cards would amount for approx. 1 billion dollars at the beginning of 2025: Still a drop in the ocean in comparison with real world payments volumes.

The missing bridge

For all the innovation that’s happened in DeFi, one thing has remained surprisingly hard paying for a coffee with your crypto wallet. In practice, the experience has looked something like this:

- Fiat and crypto rails lived in different universes. To move value you had to go through exchanges and repetitive KYC checks.

- Card issuance sat in the hands of legacy payment service providers who were not set up to plug in self custody wallets in a co mpliant way.

- Merchants did not want volatility, token tickers, or reconciliation headaches at checkout. They wanted the same thing they already had: predictable settlement, clear reporting, and chargeback processes.

The result was a first generation of “crypto cards” that were fun to tweet about and annoying to use. Many of them behaved more like prepaid vouchers than real cards, and some high profile programs got shut down when compliance and licensing reality caught up. Binance having to close its EU card program in 2023 is one example of how fragile these setups could be.

Turning on-chain balances into real-world spend

Given this backdrop, the key question is not whether people will want to pay with value held on chain. The adoption numbers suggest they already do, just indirectly. The question is which infrastructure will make that usage practical and safe.

In our view, the bridge layer between self-custody and cards had to solve four things at once:

- Real card programmes, not marketing experiments. That means handling program management, BIN sponsorship, KYC and AML flows, chargebacks, dispute management, lifecycle events and network rules in a way that regulators and issuers are comfortable with.

- Stablecoin-aware settlement. At the point of sale, the merchant expects a standard card transaction in fiat. Under the hood, the system should be able to authorise against stablecoin balances, convert at predictable rates and reconcile without manual work.

- Global coverage with regional depth. The main corridors today still run through the US and the EU, but users are spread globally. A serious platform needs to be able to launch programmes in multiple jurisdictions while respecting local constraints.

- Developer-grade tooling for wallets and fintechs. Teams that build consumer wallets, payment apps or neobanks want APIs, webhooks, dashboards and clear SLAs, not custom one-off integrations with each issuer or processor.

Where stablecoins and cards quietly converge

If global digital payments are a trillion dollar flow each year, and stablecoins already settle volumes on the order of Visa and ACH combined, the overlap between those two worlds is not a side quest. It is a core part of how the financial system of the next decade will move money.

Most institutional discussions around tokenisation still focus on securities, funds and wholesale settlement. That is important, but everyday payments are where users interact with money most often. Bringing self-custody and stablecoin balances into that loop is a way to:

- Raise the utility of tokenised assets beyond “parked yield”.

- Shorten the path between on-chain liquidity and real-world spending.

- Give issuers, treasurers and regulators a live testbed for programmable money in a familiar card format.

From our perspective, this checks all the boxes of how web3 payments should feel like:

- It reduces friction where Web3 meets real-world usage.

- It is directly exposed to regulatory clarity in the US and EU instead of trying to route around it.

- Revenues can scale with transaction volume through interchange and software fees, which is a model the market understands.

The story here is not that “everyone will pay with crypto tomorrow”. The story is that the global payments system is already mostly digital, stablecoins have quietly become a large settlement layer, and regulation in the US and EU is starting to give those instruments a clear legal home.

In that context, making self-custody wallets usable at the same terminals and online checkouts people already trust feels less like a speculative bet and more like normalising an obvious missing piece.

We think that is good for users, for issuers and, over time, for the resilience and efficiency of the broader financial system as well as opening up a world where self custody enables individuals to be their own banks for their everyday life especially in areas where banking is still a luxury that many cannot afford.

If adoption really pick-up the numbers get interesting pertty fastfast. Using the ECB’s H2-2024 baselines as a proxy, the euro area ran about 77.6 billion non-cash payments in that half, with cards at 57% and an average card ticket around €39 in H1-2024. Annualized, that implies roughly 88–90 billion card transactions and €3.3-3.6 trillion of card GMV.

If stablecoin-funded wallets take just 1–3% of those transactions by the 2027–2028 window, you are looking at ~0.9–2.7 billion transactions and €30–€110 billion of spend flowing from programmable balances into standard card acceptance. At typical issuer/processor economics of ~50–80 bps, that supports a €150–€900 million annual revenue pool before SaaS and value-added fees, with further upside as cross-border spreads compress and dispute overheads drop. This scenario is not outlandish given stablecoins already clear on the order of $9 trillion over the last twelve months and touched roughly $1.25 trillion in September 2025 alone, which suggests the funding rail is already operating at payments scale.

The team building that bridge: Kulipa

At Blockwall we have been lucky to partner with an outstanding team ‘(👋 Axel and Michael) in that field, sharing the same vision and bringing field experience from well established companies like Mastercard, Binance or Whatsapp.

Kulipa builds a payment stack that lets wallets, stablecoin-native fintechs and more traditional financial apps issue cards that spend directly from digital assets, while presenting as normal Mastercard debit or prepaid cards to merchants. Under the hood they handle program management, EMI partnerships, KYC and AML flows, card lifecycle and reconciliation, and they expose all of this through APIs, webhooks and an operations dashboard.

On the product side, their initial deployments focus on stablecoin spending from self-custody wallets like Solflare or Ready. A card transaction triggers a conversion from stablecoins to fiat at the terminal, with no extra integration needed for the merchant also supporting Apple Pay or Google Pay for users.

In other words: they make crypto spendable.

It’s a deceptively simple idea, but one that has technically and operationally been hard to execute and we’re excited to see what next under their sleeves! 🔥💳

Disclaimer

To avoid any misinterpretation, nothing in this blog should be considered as an offer to sell or a solicitation of interest to purchase any securities advised by Blockwall, its affiliates or its representatives. Under no circumstances should anything herein be interpreted as fund marketing materials for prospective investors considering an investment in any Blockwall fund. None of the data and information constitutes general or personalized investment advice and only represents the personal opinion of the author. The author and/or Blockwall may directly or indirectly be exposed to the mentioned assets/investments. For further information please view the full Disclaimer by clicking the button below.

This work is licensed under the Creative Commons Attribution – No Derivatives 4.0 International License. CC BY-ND 4.0 Legal Code | Creative Commons