Blockwall's Year in Review 2025

Dear Founders, Investors, and Friends,

As we approach the end of 2025 and another holiday season, we want to take a moment to thank you for your continued trust and support. This year has been intense, at times volatile, and ultimately defining for the maturation of crypto, digital assets, and Web3 as an investable asset class.

Across our LP base, portfolio, and broader network, we feel privileged to partner with people who are building and allocating with a long-term view. Your conviction and collaboration are what make our work possible.

In this “Year in Review”, we revisit the most important developments of the past twelve months and highlight how they have shaped our strategy at Blockwall. We also reflect on the progress we have made as a firm and outline how we plan to allocate capital, grow our capabilities, and support founders in the years ahead.

We wish you and your families a peaceful holiday season and a healthy, successful start into the new year.

Table of Contents

- Highlight Summary

- 2025: A New Era for Crypto and Web3

- Private, Public, and M&A Market Overview

- Reflections on Our Growth in 2025

- The Road Ahead

Highlight Summary

2025 marked a structural turning point for crypto and Web3. After several years shaped by regulatory uncertainty and uneven market conditions, the environment shifted toward clarity, execution, and institutional participation.

In the U.S., the change in regulatory stance replaced enforcement-driven ambiguity with defined frameworks for stablecoins and market structure. In Europe, MiCA fully went live and policymakers moved to make tokenized capital markets viable at scale. Together, these developments reduced one of the industry’s most persistent risks and created a more predictable operating environment for companies and investors.

This clarity translated into tangible adoption. Stablecoins moved beyond crypto-native use cases into payments, treasury, and settlement, with banks, fintechs, and global enterprises deploying them at scale. Tokenization followed a similar path, led by money market funds, public-sector participation, and early capital markets pilots that demonstrated onchain finance is moving from experimentation into production. Across private and public markets, activity returned in a more disciplined form, marked by selective capital deployment, consolidation, and renewed access to institutional distribution.

Within this context, Blockwall continued to scale as an early-stage platform. Fund I was fully repaid at a 5.5x net DPI, placing it among the top-performing venture funds globally of its vintage. Fund II progressed into a phase where a growing share of the portfolio entered scaling stages and secured follow-on capital, while Fund III completed its first close and began deployment.

A key enabler of this scale has been X-Ray, Blockwall’s proprietary AI-powered sourcing engine. X-Ray allows us to systematically scan the global Web3 founder landscape, identify relevant teams earlier, and engage founders proactively. By embedding data and automation into our sourcing process, we significantly expanded deal flow and geographic reach while keeping the core team deliberately lean.

Looking ahead, the industry is entering a phase where foundational infrastructure is being built, regulatory frameworks are in place, and institutional participation is still in its early innings. Historically, this combination has created some of the most attractive conditions for early-stage investing. Blockwall is positioned to operate in this environment with a proven track record, a maturing portfolio, and a scalable sourcing platform designed to capture opportunities early as this next phase unfolds.

2025: A New Era for Crypto and Web3

A Regulatory Turning Point in the U.S.

The year began with a decisive shift in U.S. policy. Under the new administration, regulators moved from regulation-by-enforcement to actively shaping new regulatory frameworks.

The GENIUS Act progressed from proposal to law, creating the first federal framework for fully reserved, supervised stablecoins.

The CLARITY Act advanced in parallel, offering a clearer boundary between securities and commodities, and thus providing a clear division of oversight between SEC and CFTC. Bank regulators followed suit: the OCC explicitly allowed banks to custody crypto, issue stablecoins and run nodes, while the FDIC withdrew earlier restrictive guidance. At the same time, high-profile enforcement actions against Coinbase, Uniswap, Consensys, Robinhood and others, were dropped or dismissed.

Regulatory uncertainty, for a long time the main brake on widespread institutional and enterprise participation, finally gave way to a predictable operating environment.

In parallel, Europe made its own structural leap.

MiCA fully went live, giving the EU its first unified rulebook for stablecoins and crypto service providers. In addition, the European Commission proposed a major overhaul of the DLT Pilot Regime to make tokenized capital markets viable at scale.

The goal is to remove the early constraints that kept participation low, open the framework to a wider range of financial institutions, and create the conditions for large-scale issuance, trading and settlement of tokenized securities.

Crucially, the reforms would also allow Europe’s major market infrastructures to adopt DLT-based settlement without overhauling their entire regulatory setup.

With both the U.S. and the EU now defining, rather than resisting, crypto’s operating rules, the conditions for institutional adoption became materially stronger.

Stablecoins Move Into Mainstream Finance

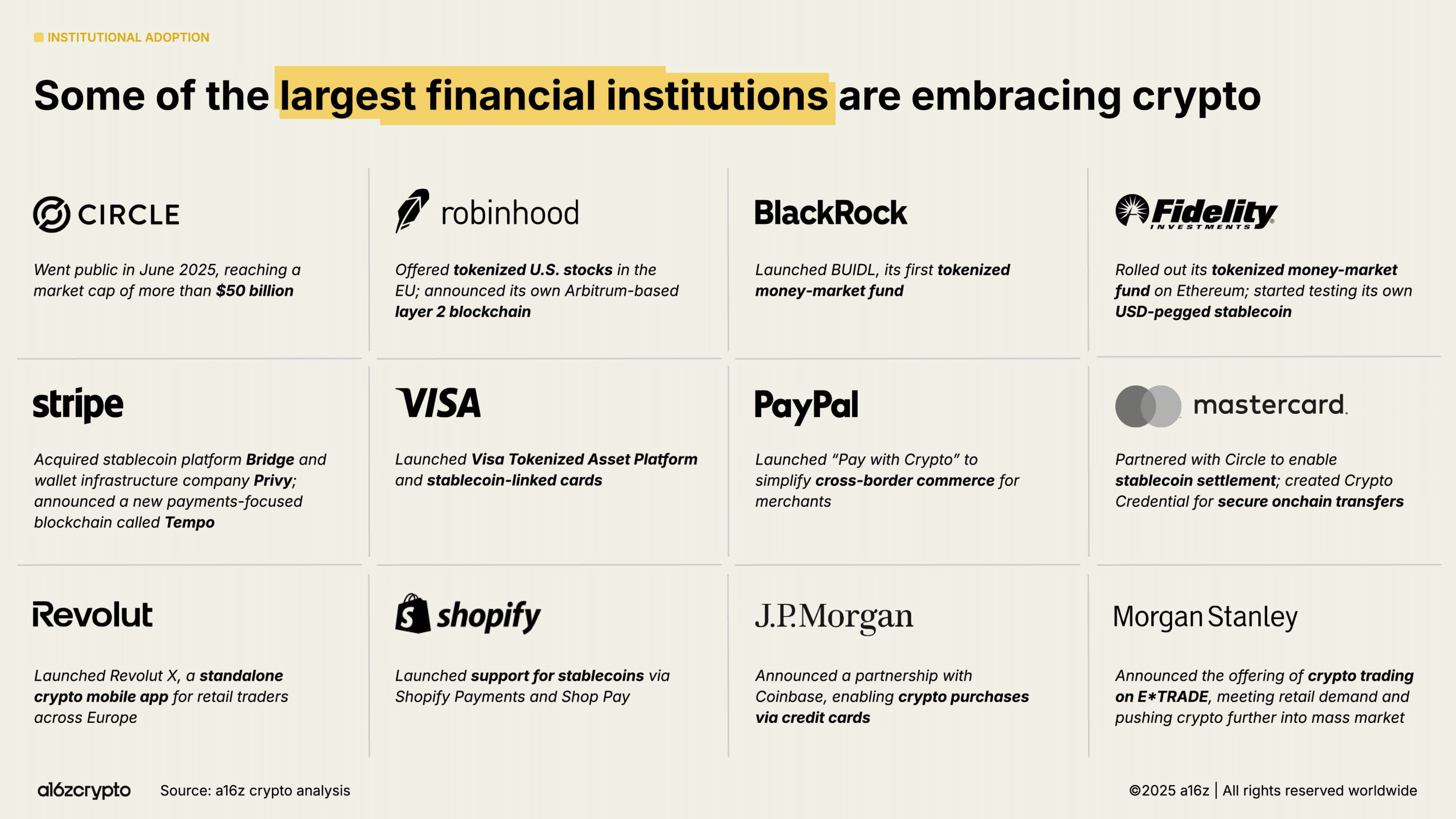

Regulatory clarity immediately unlocked adoption. Institutions and fintechs are no longer just circling the space. Visa, PayPal, Mastercard, and Shopify are all actively exploring, building, or launching stablecoin-related products.

JPMorgan, for example, issued JPMD, the first deposit token from a global bank on a public blockchain. Major enterprises like Sony and Siemens continued to run real-world settlement pilots.

Some payment companies went even further: Fintech-giant Stripe embedded stablecoins into its core infrastructure and revealed the development of Tempo, its own Layer 1 network built for high-throughput stablecoin payments, which is expected to go live next year.

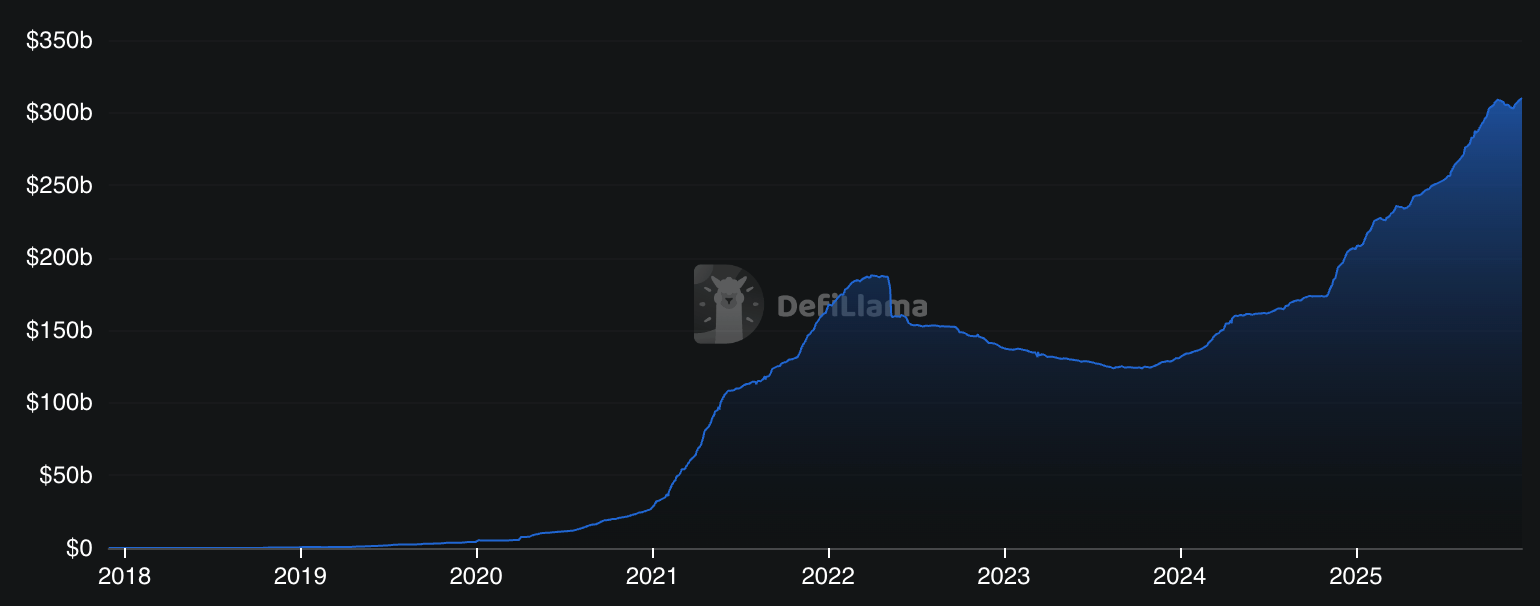

In terms of actual growth numbers, stablecoins also had one of its best years so far in 2025. Total market capitalization of stablecoins grew by 50% to around $310 billion.

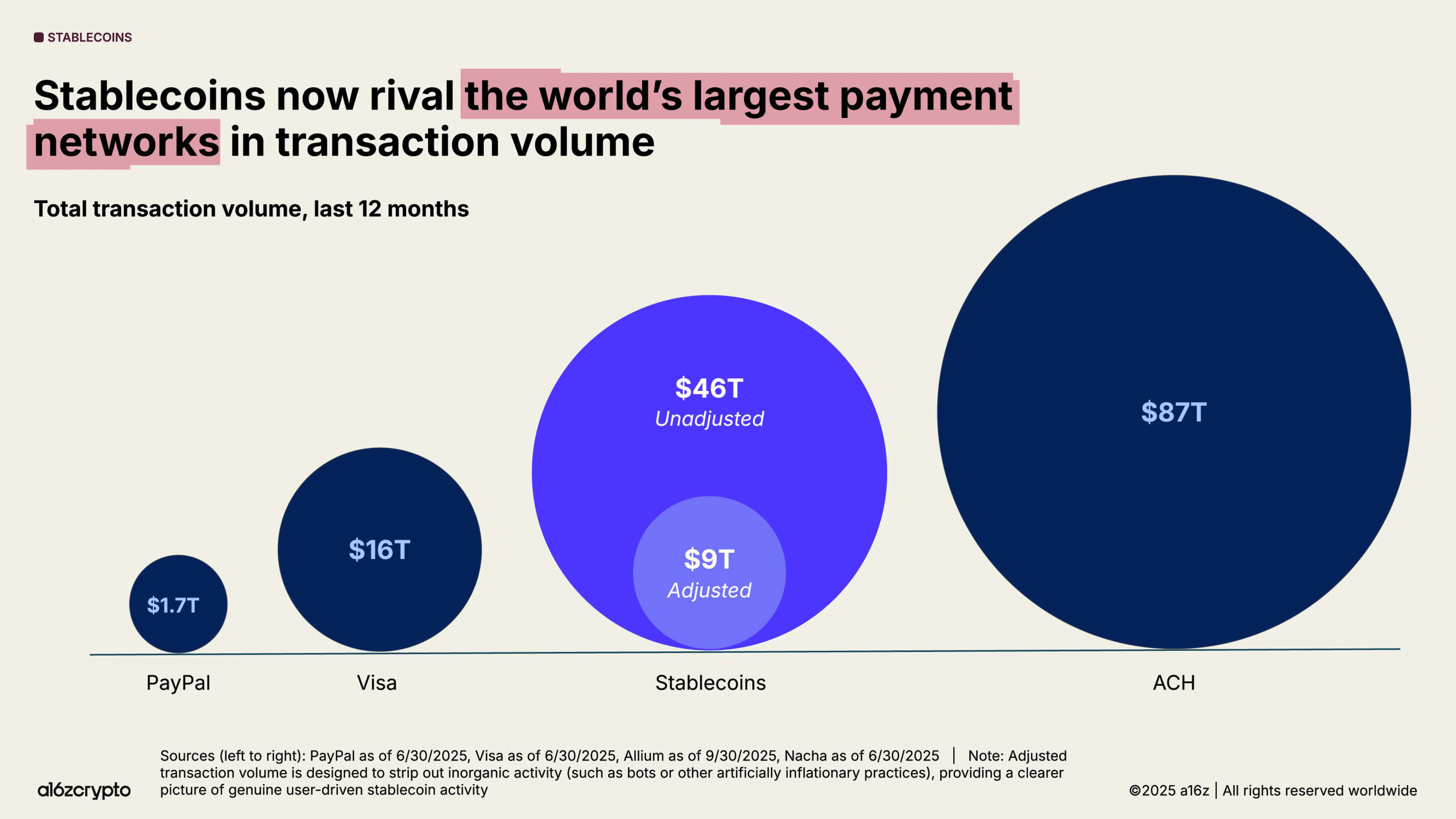

Stablecoins also processed $46 trillion in transactions last year (around $9 trillion adjusted for real use), which is more than Visa and PayPal combined.

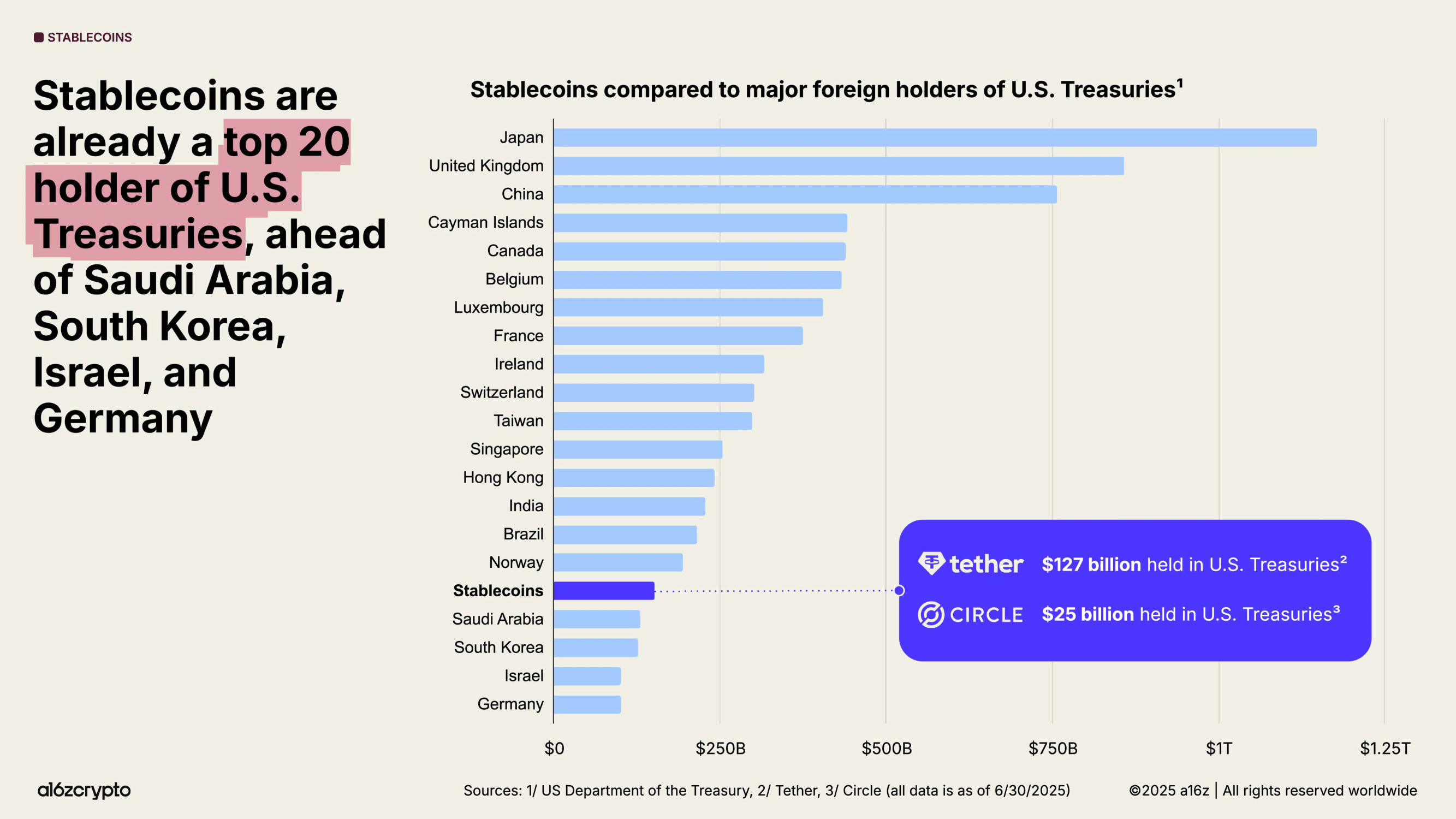

Stablecoin issuers now hold $152 billion in U.S. Treasuries, ranking above Germany and South Korea, making them politically significant to the U.S. government.

These figures make it clear that stablecoins are no longer a crypto-native phenomenon, but a building block of global payment and treasury systems.

Tokenization Reaches the Core of Capital Markets

Tokenization followed the same trajectory. The most mature use case, tokenized money market funds, became a true anchor for institutional activity.

In Europe, Banque de France executed onchain repos using tokenized MMFs, and Bpifrance allocated part of its balance sheet into a tokenized euro MMF issued by Spiko, a Blockwall portfolio company, which demonstrates that public institutions now feel confident interacting with tokenized instruments directly.

Speaking of Spiko: Beyond being named “Startup of the Year” at AMTechDay, one of Europe’s premier conferences for innovation in the asset management industry, the company saw rapid adoption. This year alone, its assets under management grew from around $130 million to more than $600 million, making it the leading European issuer of tokenized money market funds and one of the largest globally.

In the U.S., capital markets infrastructure also began to shift. DTCC launched a blockchain-powered collateral platform as a pilot designed for institutional settlement. Google, through its DLT pilots with CME and other financial institutions, further signaled that tokenization is becoming part of mainstream market infrastructure.

At the same time, platforms like Kraken and Robinhood introduced onchain stocks and ETFs, which are tokenized wrappers that provide price exposure to underlying equities. These instruments do not confer shareholder rights and are not native issuances, but they represent an important transitional step. They also show early demand, since the total value of tokenized stocks grew from nearly zero to roughly $550 million since July.

With companies like Superstate in the U.S. actively working toward native onchain equities, we expect strong continued growth in this vertical and the first fully tokenized issuances as early as next year.

Private, Public, and M&A Market Overview

Private Markets

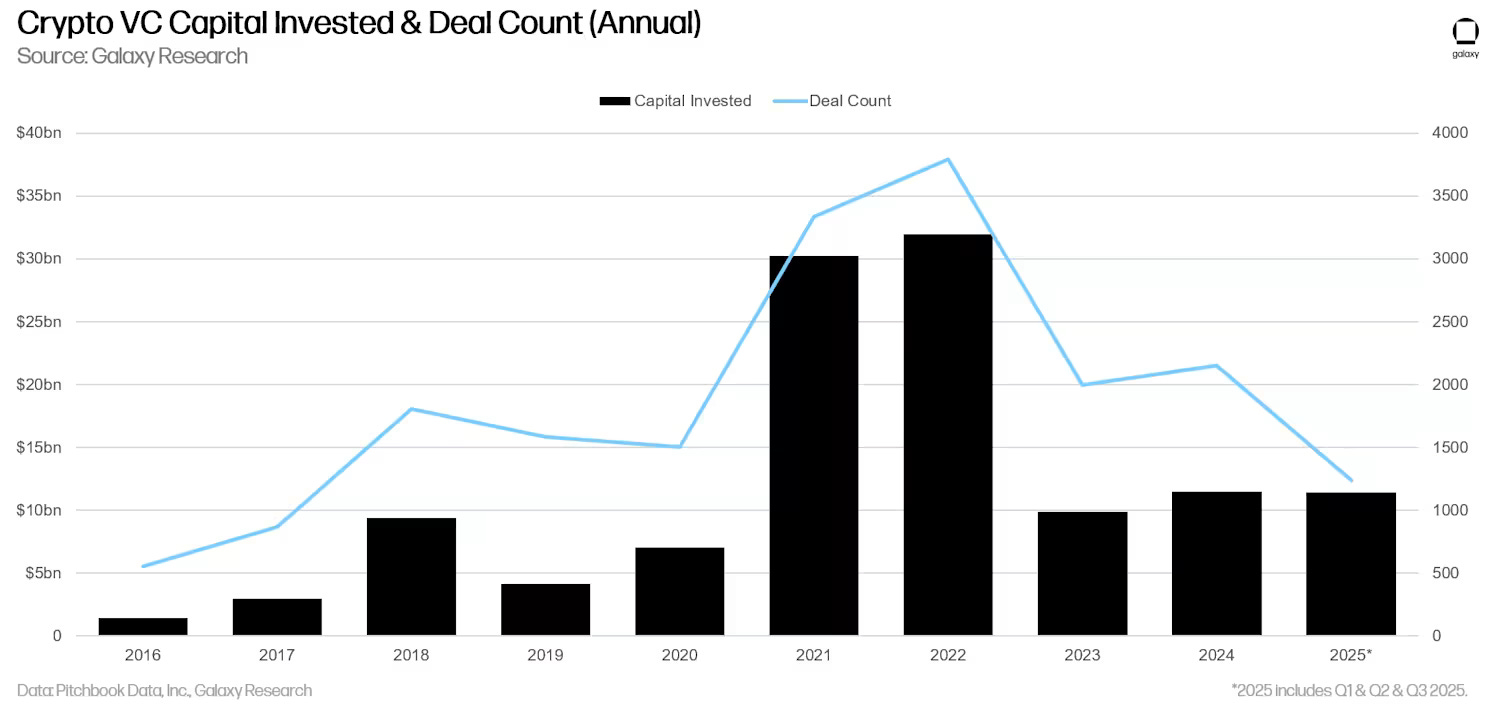

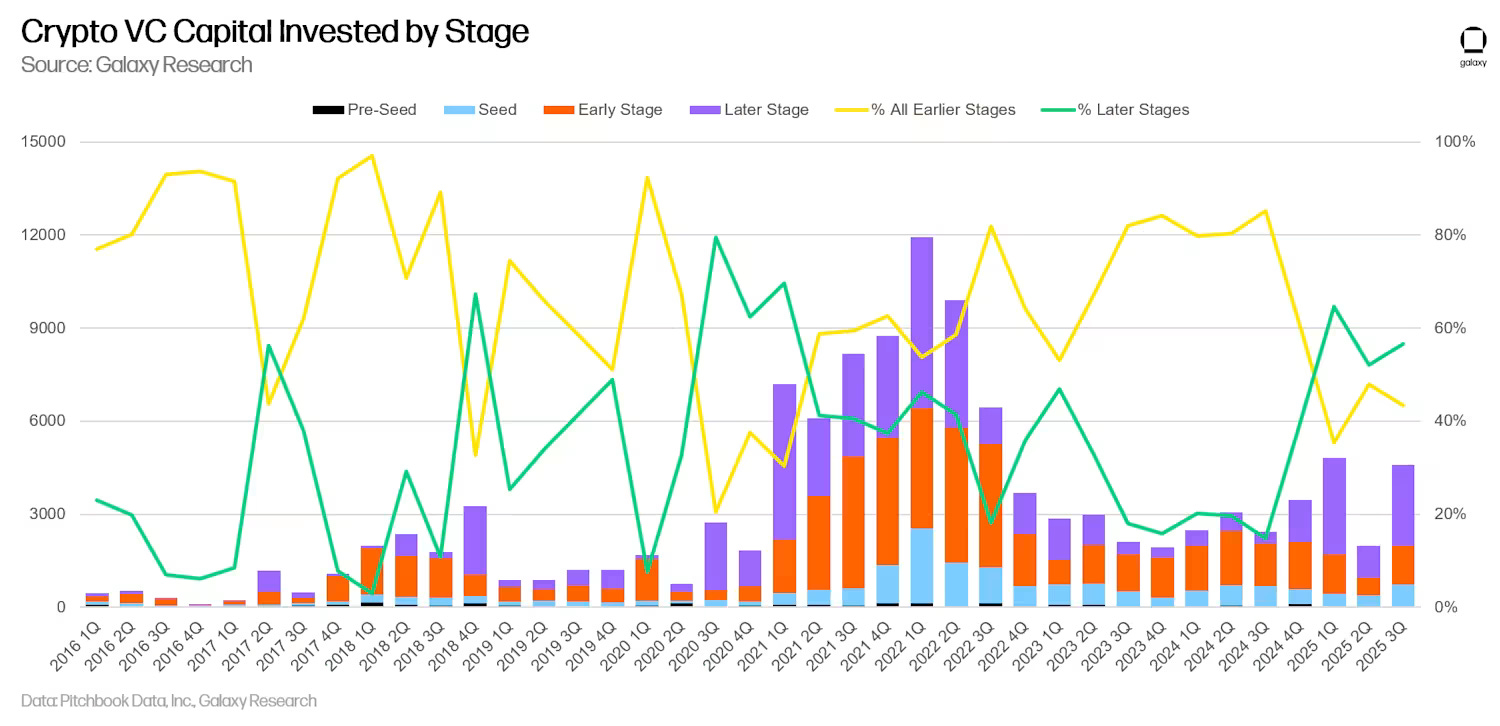

Crypto startups saw a healthy flow of capital in 2025. Total crypto VC investment currently stay at roughly $13 billion year-to-date and is projected to close the year between $18-25 billion, making 2025 the strongest year since the 2021-2022 boom, albeit still below peak levels.

Capital deployment skewed toward more mature companies. Throughout the year, around 56-57% of invested capital went into later-stage rounds (Series B and beyond), compared to 43-44% into early-stage ventures. This marks a shift from prior years and reflects the continued maturation of the industry.

At the same time, early-stage activity remained resilient. Pre-seed and seed deal counts held steady, signaling sustained founder activity and continued new company formation.

Overall, the venture market in 2025 was characterized by disciplined growth. More capital returned to the space, but with a clear preference for proven teams and scalable business models.

Global Regional Trends

Venture investment remained geographically diverse but U.S.-led. The United States accounted for roughly 30% to nearly 50% of global crypto VC deployment in each quarter. At the same time, the rebound was global, with strong activity in regions benefiting from increasing regulatory clarity, particularly Europe and Asia-Pacific.

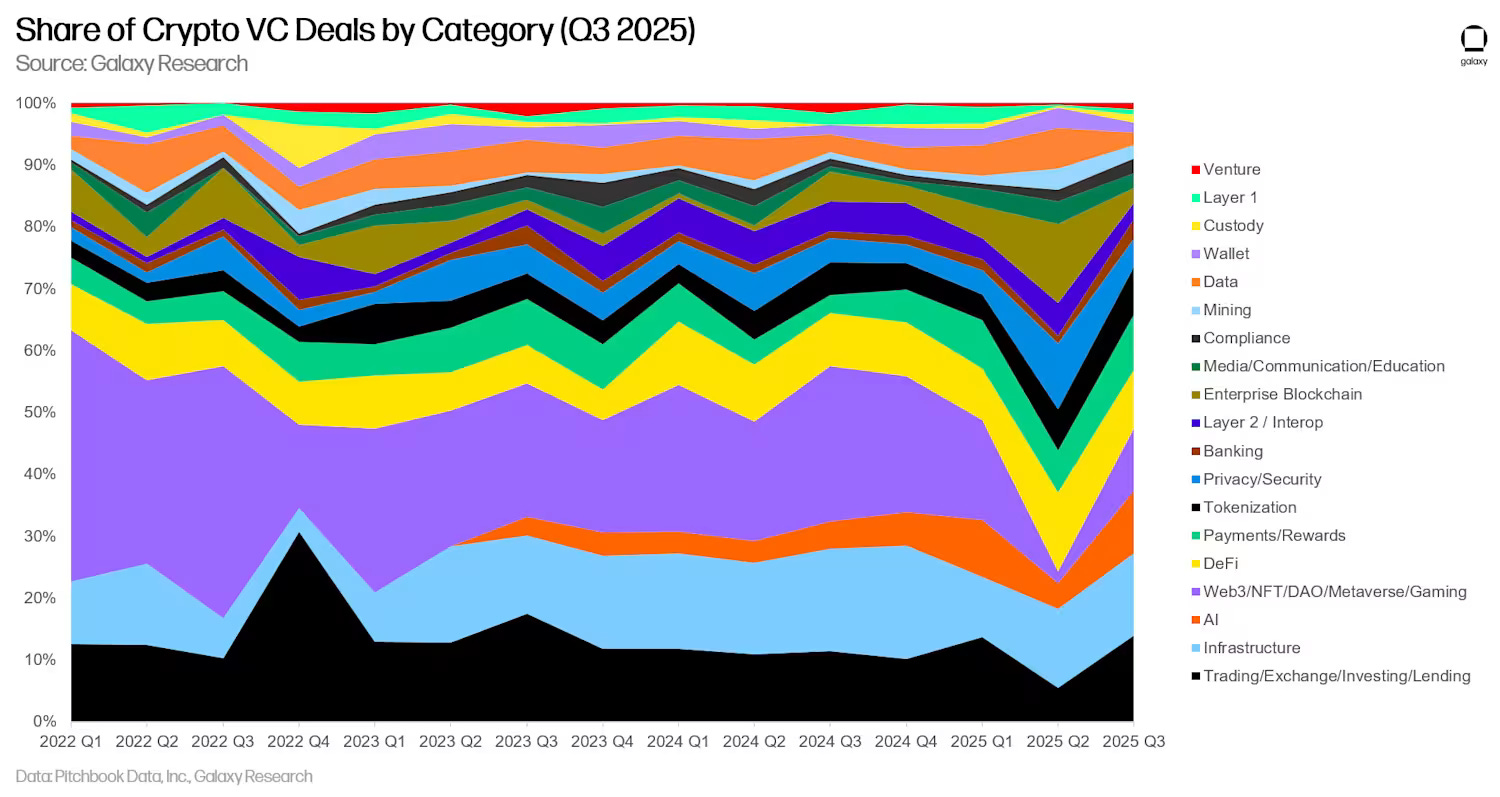

Sector Trends

Capital concentrated in sectors aligned with compliance, scalability, and institutional use cases. Centralized exchanges, brokerage and fintech platforms, blockchain infrastructure (Layer 1 and Layer 2 technologies, staking services), and payments and stablecoin-focused applications attracted the majority of funding. In contrast, investment in entertainment and purely speculative crypto applications continued to decline, underscoring a clear shift toward utility-driven models.

Public Markets

Crypto markets experienced a strong rally in 2025. In July, total cryptocurrency market capitalization surpassed $4 trillion for the first time. Bitcoin led the move, breaking above $120,000 in July and reaching a new all-time high of around $126,000 in early October.

In Q4, markets corrected as profit-taking coincided with rising macro uncertainty. Higher oil prices and a more cautious stance from the Federal Reserve tempered the risk-on environment. As a result, the market is expected to close the year slightly below mid-year highs, around $3.0 trillion, compared to roughly $3.4 trillion at the start of the year.

Crypto IPOs and Public Listings

2025 marked a breakthrough year for crypto companies accessing public equity markets. In June, Circle, the issuer of USDC, completed a landmark IPO on the NYSE. The offering was among the best-performing IPOs of the year, with strong aftermarket performance that clearly demonstrated renewed investor appetite for crypto and digital asset businesses.

Momentum carried into August, when Bullish, an institutional-focused crypto exchange operator, also went public in New York. Like Circle, the listing was well received and reinforced the view that public markets were once again open to crypto-native companies. Together, these IPOs helped reopen the public markets for the sector and encouraged additional players to follow suit, including firms such as Gemini and other digital asset platforms exploring or initiating listing processes.

Since then, share prices have retraced alongside broader market volatility, and investor sentiment has cooled. This raises an open question for the year ahead: whether the IPO window remains meaningfully open, or whether public market activity will moderate as valuations normalize and market conditions become more selective.

Beyond IPOs, the year also marked deeper mainstream integration. Coinbase was added to the S&P 500, and policy discussions advanced around allowing crypto exposure within 401(k) retirement plans.

Record Year for Crypto M&A

Industry consolidation accelerated meaningfully in 2025. By late November, announced crypto M&A deal value reached $8.6 billion across 133 transactions, according to PitchBook, marking a record year for the sector.

Notable transactions included:

- Coinbase acquiring Deribit for $2.9 billion

- Kraken acquiring NinjaTrader for $1.5 billion

- Ripple acquiring Hidden Road for $1.25 billion

This surge in M&A activity reflects a maturing industry, with leading players using consolidation as a strategic growth lever amid clearer regulation and improved market conditions.

ETFs and Investment Products

Crypto investment products experienced record inflows in 2025. Year-to-date net inflows into digital asset ETPs exceeded $45 billion, surpassing prior annual records, with Bitcoin and Ether products capturing the vast majority of demand. Assets under management across global crypto ETFs and ETPs peaked near $260 billion mid-year before retracing in Q4 alongside broader market corrections to around $180 billion as of December.

Product breadth also expanded meaningfully, with around 340 crypto ETP products being live globally at of December.

A key inflection point came in early fall, when U.S. regulators approved a streamlined, generic listing framework for digital asset ETFs. This materially shortened approval timelines and enabled faster market entry.

As a result, the final quarter of the year saw the first spot ETFs tied to large-cap altcoins such as Solana and XRP, alongside early multi-asset products. This regulatory shift sets the stage for a broader wave of digital asset ETFs in 2026, significantly expanding institutional access beyond Bitcoin and Ether.

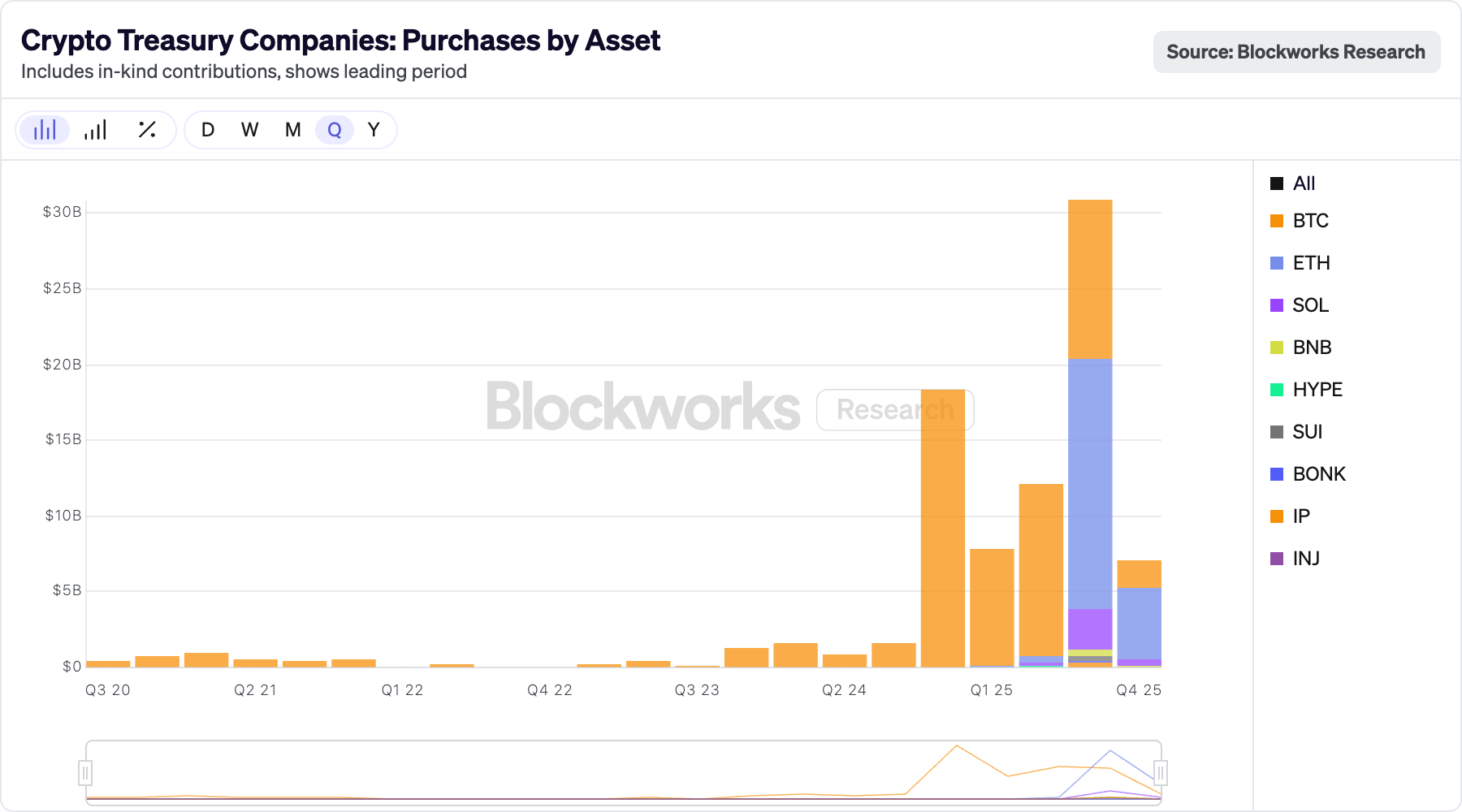

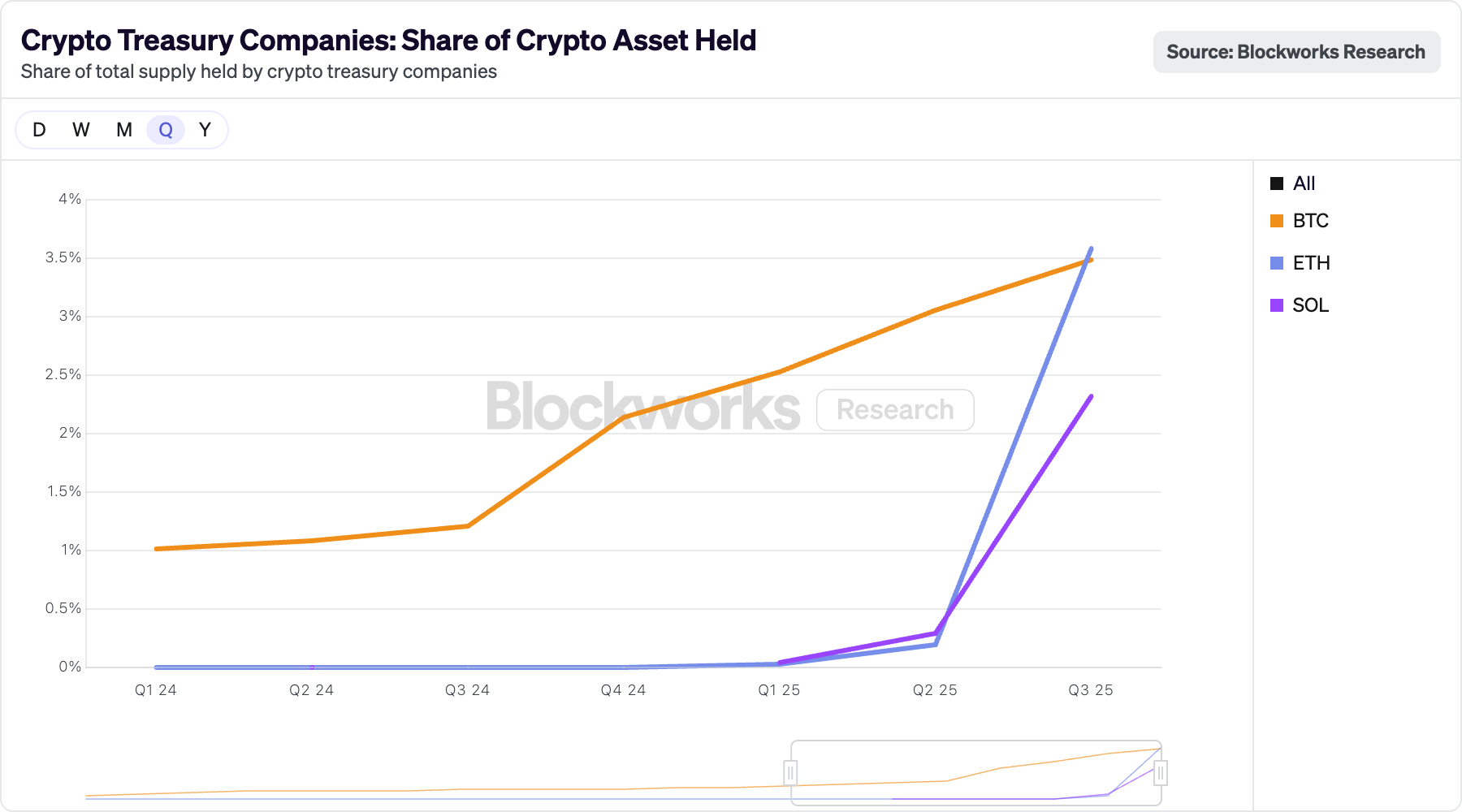

Digital Asset Treasury Companies

In 2025, digital asset treasury (DAT) companies emerged as an important marginal buyer of major crypto assets, reinforcing price momentum during the rally. Alongside rising ETF flows, these vehicles offered public market investors an alternative way to gain exposure to crypto through equities, often with embedded leverage to the underlying assets held on the balance sheet.

- Reminder: The DAT model traces back to Strategy under Michael Saylor, which began accumulating Bitcoin in 2020 by issuing equity and convertible debt and deploying the proceeds into BTC. The objective is to increase crypto holdings per share over time by using public market access to continuously expand the balance sheet. Strategy’s early success, including periods of equity outperformance relative to Bitcoin, turned this approach into a widely copied playbook.

That playbook scaled rapidly this year. Strategy remained the dominant player, holding roughly $60 billion in Bitcoin, equivalent to around 2% of total BTC supply by mid-December. Ethereum followed a similar path. BitMine emerged as the largest ETH-focused treasury company, holding roughly 2% of ETH supply, valued at approximately $11 billion. Smaller treasury strategies also formed around assets such as Solana, signaling experimentation beyond Bitcoin and Ether.

Into the year-end, however, the model entered a more uncertain phase. As both crypto prices and equity valuations corrected, access to fresh capital tightened. With continued accumulation dependent on favorable market conditions, digital asset treasury companies now sit at an inflection point, as investors assess whether the strategy represents a durable structural feature of crypto markets or a short-term phenomenon closely tied to the current cycle.

Reflections on Our Growth

This year, we continued professionalizing and scaling Blockwall across all dimensions.

Our Funds

2025 marked an important milestone for us. We fully repaid Fund I at a net DPI of 5.5x, placing us among the top 5% of global venture funds of our vintage.

Fund II continued its strong development throughout the year. We now count 24 investments in the portfolio, several of which achieved significant follow-on rounds in 2025, including Spiko and Validation Cloud, both raising their Series A rounds. Many companies have entered the scaling phase, and we are approaching the final stretch of the Fund II investment period.

In parallel, we executed the first closing of Fund III end October and now have approximately €22.5 million closed, and we already signed the first investment of the new fund. Our target remains €50 million, and we expect continued momentum over the coming months.

Scaling through AI: Introducing X-Ray

Last year, we recognized the operating leverage that AI can introduce into early-stage investing. This is why one of our core strategic priorities has been building X-Ray, our proprietary AI-powered sourcing engine designed to systematize how we scan the global Web3 founder landscape.

In 2025, X-Ray moved from an internal experiment to the backbone of our global deal flow:

- This year we doubled our annual deal flow and screened more than 5,500 startups. Roughly 70% of these opportunities, around 3,800 in total, came from outbound sourcing driven by X-Ray.

- X-Ray has fundamentally reshaped our funnel. Instead of relying on inbound references, we can now reach founders proactively and engage with them much earlier in their journey.

- As of today, the system tracks >170,000 profiles globally and organizes them into a dynamic social graph that highlights meaningful signals.

To further accelerate X-Ray’s development, we are increasing our engineering capacity and will bring a full-time AI engineer on board early next year.

Web3 Handbook

In July, after months of focused research and writing, we published our Web3 Handbook. It provides a structured overview of the Web3 landscape, not from a technical or academic angle, but from the perspective of an active investor or curious reader looking to understand the core ideas shaping the ecosystem.

Although long-form (around a 90-minute read), it remains a high-level introduction that you can read end to end or explore selectively. It does not attempt to cover every aspect of Web3, but highlights the themes we consider most relevant today. If you missed it, you can find it here.

Research Highlights

In addition to our published Web3 Handbook and building on last year’s efforts, we once again published some of our own research and shared more insights about our investments this year.

Some Highlights include…

- An overview of (Re)Staking pt2

- DeFi Needs a Jony Ive Moment: Why We Invested in Rebind

- From keys to cards, bridging self-custody and everyday payments

- Stablecoins: The Internet’s Financial Base Layer

Investments We Made

This year, we signed nine deals, with one of them to be announced at a later date:

- Rebind: A mobile-first, non-custodial DeFi app that makes it effortless to buy crypto and access curated on-chain yield strategies through simple social logins and passkeys. See here on why we invested.

- Blu: An onchain neobank serving the 47.5 million unbanked people across LATAM, giving them access to credit cards and a way to build a real financial identity.

- Kirha: An infrastructure gateway for the emerging Model Context Protocol (MCP), an open standard enabling large language models to access real-time, structured data sources and compensate providers via blockchain-based micropayments.

- Spectarium: Game developer, who is building a cross-platform, gameplay-first action RPG inspired by global mythologies, delivering a Web2-level experience that uses Web3 only where it truly adds value: ownership, trading, and community.

- Den: Developer of an end-to-end wallet solution to manage onchain funds and increase security, enabling enterprise-grade onchain custody.

- Kulipa: Provider of white-label crypto card infrastructure for self-custodial wallets, enabling users to spend stablecoins directly from their wallets without relinquishing custody, bridging on-chain assets with real-world payments. See here why we invested.

- Yousend: A stablecoin-based remittance platform enabling fast, low-cost cross-border transfers between North America, Europe, and key African corridors.

- Flyra: Developer of “the Banking OS” for migrants. Essentially, it’s an all-in-one system designed for global workers and their families, where money lives and moves easily. They can store it, spend it, borrow when needed, and even grow it.

Blockwall Investor Summit

A major highlight of the year was our 3rd investor summit in Frankfurt, where we brought together an incredible group of investors, founders, and industry leaders.

The summit was a platform for deep discussions about Web3, crypto, finance, and the future of the internet, and it sparked meaningful conversations about where the industry is headed.

To get an impression of the summit, please see our trailer here.

And for those looking to dive deeper into the conversations, below you can find the list of all panels, fireside chats, and keynotes:

- Institutional-Ready: Web3 goes Mainstream — with Bert Staufenbiel (KfW), Ivan de Lastours (Bpifrance), Christoph Hock (Union Investment), and Torsten Hunke (VanEck Europe). You can view the full panel here.

- Future of Banking in an Onchain World — with Manfred Knof (Commerzbank), Mathias Imbach (Sygnum Bank). You can view the full panel here.

- Web3’s Potential to Disrupt and Building Animoca into a Billion USD Company — with Yat Siu (Animoca Brands). You can view the full fireside chat here.

- The Future of Capital Markets — with Paul-Adrien Hyppolite (Spiko), Michael Duttlinger (Cashlink), Hendrik König (Bankhaus Metzler). You can view the full panel here.

- Stablecoins: Instant, Compliant, Programmable — with Dorothea Ysenburg (Mastercard), Alexander Hoeptner (AllUnity), Casper Yonel (Blu Financiero), Christopher Beck (tradias). You can view the full panel here.

- Founder Spotlight — with:

- Paul-Adrien Hyppolite (Spiko). You can watch the spotlight on Spiko here.

- Casper Yonel (Blu). You can watch the spotlight on Blu here.

- Gaia Ferrero Regis (Byzantine). You can watch the spotlight on Byzantine here.

- Steven Figura (Rebind). You can watch the spotlight on Rebind here.

- Romain Schneider (Spectarium). You can watch the spotlight on Spectarium here.

- Axel Cateland (Kulipa).You can watch the spotlight on Kulipa here.

- From Investor to Operator — with Arjun Sethi (Kraken). You can watch the full fireside chat here.

Thank you to everyone from the Blockwall team who made this possible: Jannis Choulidis, Nikos Choulidis, Damien Roch, Max Schneider, Syed Armani, Leonard Lang, Havard Rivedal, Bjarmi Leo, Lars Singbartl, and Lisa Bourcarde.

For anyone who couldn’t attend: Over the coming weeks and months, we’ll be sharing more content and highlights of the Summit with you. To stay in the loop, feel free to follow our Blockwall account on LinkedIn.

The Road Ahead

Looking into next year, our priorities are clear.

On the fund side, we expect to complete the investment period of Fund II by mid-year and to increasingly concentrate on follow-on rounds, as more portfolio companies transition from early traction into scaling phases. In parallel, we will continue deploying Fund III and work toward the €50 million target fund size mentioned earlier, with a selective, high-conviction approach.

At the same time, we will keep strengthening Blockwall’s technical capabilities. A key focus will be the continued expansion of X-Ray, further embedding data, automation, and AI into our sourcing and market analysis. Our main goal remains to identify strong teams early and maintain a systematic, global view of the opportunity set as the market scales.

From a market perspective, we remain constructive. Regulatory clarity in the U.S. and Europe has materially improved the environment for institutional adoption, and we expect this to continue driving activity in stablecoins, tokenization, and onchain financial infrastructure. As these building blocks mature, we also expect DeFi activity to reaccelerate, supported by deeper liquidity and more institutional as well as fintech/ enterprise participation.

Overall, we see the year ahead as one of execution and expansion. The foundations have been laid, and both the market and our portfolio are moving into a phase where scale, discipline, and focus will matter most.

Disclaimer

To avoid any misinterpretation, nothing in this blog should be considered as an offer to sell or a solicitation of interest to purchase any securities advised by Blockwall, its affiliates or its representatives. Under no circumstances should anything herein be interpreted as fund marketing materials for prospective investors considering an investment in any Blockwall fund. None of the data and information constitutes general or personalized investment advice and only represents the personal opinion of the author. The author and/or Blockwall may directly or indirectly be exposed to the mentioned assets/investments. For further information please view the full Disclaimer by clicking the button below.

This work is licensed under the Creative Commons Attribution – No Derivatives 4.0 International License. CC BY-ND 4.0 Legal Code | Creative Commons